A bank account is one of the most important financial tools in daily life. People use it to receive salaries, save money, pay bills, and transfer funds. However, many account holders do not realize that if they stop using their account for a long time, it may become inactive.

If you are wondering what happens when bank account becomes inactive, this guide will explain everything in simple language. You will learn why accounts become inactive, what problems it can create, and how to reactivate an account easily.

Understanding inactive accounts is important because ignoring them may lead to inconvenience when you suddenly need access to your money.

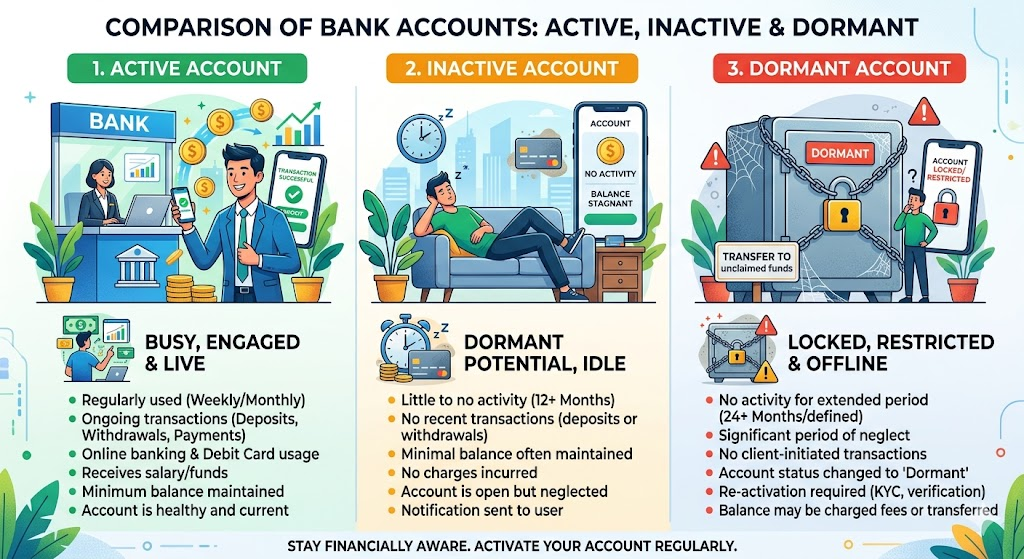

What Is an Inactive Bank Account?

A bank account becomes inactive when there are no customer-initiated transactions for a certain period. The exact period depends on the bank and country, but many banks classify an account as inactive after 12 months of no activity.

Customer-initiated transactions include:

- Depositing money

- Withdrawing cash

- Transferring funds

- Using debit cards

- Making online payments

Some activities, such as automatic interest credits by the bank, may not count as customer activity.

Banks monitor inactive accounts to improve security and comply with financial regulations.

What Happens When Bank Account Becomes Inactive?

The question many people ask is: what happens when bank account becomes inactive?

When your account becomes inactive, several changes may occur.

1. Transactions May Be Restricted

Banks often restrict certain transactions on inactive accounts. For example:

- Online banking transfers may stop working.

- Debit card usage may be blocked.

- Check payments may be rejected.

This is mainly done to protect account holders from fraud.

2. You May Need Verification to Use the Account Again

Before allowing transactions, banks may ask you to verify your identity using:

- Aadhaar card or ID proof

- PAN card

- Passport

- Updated address proof

This helps ensure that only the rightful owner accesses the account.

3. Online Banking Access May Be Limited

Some banks temporarily disable internet banking services for inactive accounts. You may have to visit a branch or update KYC details before access is restored.

4. The Money Remains Safe

One common concern is whether money disappears from an inactive account.

The answer is no.

Your funds generally remain in the account unless service charges apply according to bank rules. Banks do not take ownership of your money simply because the account became inactive.

5. Dormancy May Occur Later

If inactivity continues for a longer period—often around two years—the account may become dormant. Dormant accounts usually have stricter restrictions than inactive accounts.

Why Does a Bank Account Become Inactive?

Several situations can lead to account inactivity.

Common Reasons Include:

- Changing jobs and opening a new salary account

- Forgetting an old savings account

- Moving to another city

- Using only digital wallets instead of bank accounts

- Keeping an account only for emergencies

For example, if a person opens a salary account but leaves the job and stops using that account for over a year, the bank may classify it as inactive.

Difference Between Inactive and Dormant Accounts

Many people confuse inactive and dormant accounts. Although related, they are not always the same.

| Feature | Inactive Account | Dormant Account |

|---|---|---|

| Period of No Activity | Usually 12 months | Usually 24 months |

| Restrictions | Limited | More strict |

| Transaction Access | Partially restricted | Mostly blocked |

| Reactivation Process | Easier | May require more verification |

Always check your bank’s specific policy because rules can differ.

Problems Caused by an Inactive Account

An inactive account may create unexpected issues.

Delayed Access to Funds

Imagine needing emergency money only to discover that your account has been restricted. Reactivation can take time.

Missed Payments

Automatic payments linked to the account may fail, such as:

- EMI payments

- Utility bills

- Subscription charges

If you have loans connected to the account, missed payments could affect your finances.

For example, missing an EMI can sometimes impact your credit history. You may also want to read our guide on how credit scores work and why they matter.

KYC Compliance Issues

Banks periodically require customers to update Know Your Customer (KYC) information. If details are outdated, reactivation may become more difficult.

Difficulty Receiving Funds

Salary credits or transfers may be delayed if account restrictions apply.

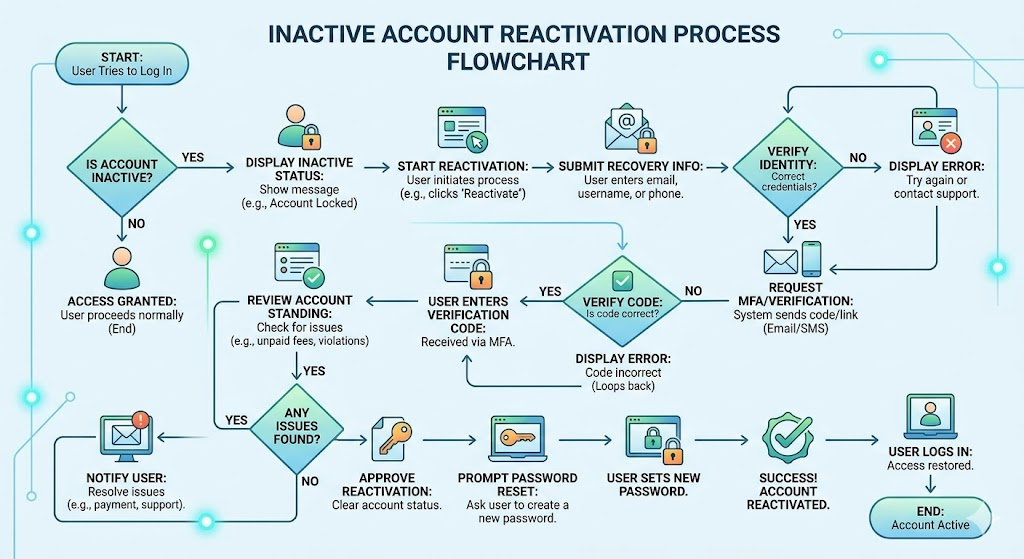

How to Reactivate an Inactive Bank Account

The good news is that reactivating an inactive account is usually straightforward.

Step 1: Contact the Bank

Visit your bank branch or customer service center.

Some banks also allow online requests.

Step 2: Submit Identification Documents

You may need:

- PAN card

- Aadhaar card

- Passport

- Address proof

Step 3: Update KYC Information

If your address, phone number, or email changed, update them with the bank.

Step 4: Perform a Transaction

After verification, the bank may ask you to perform a transaction such as:

- Depositing money

- Withdrawing cash

- Making an online transfer

This helps reactivate the account.

Step 5: Check Online Banking Access

Once reactivated, verify that:

- Mobile banking works

- Debit cards are active

- Internet banking is accessible

Tips to Prevent Your Account from Becoming Inactive

Preventing inactivity is easier than reactivating an account.

Use the Account Regularly

Make small transactions every few months.

Examples include:

- Transfer a small amount

- Use the debit card

- Deposit funds

Enable Alerts

Activate SMS and email notifications to monitor account activity.

Keep KYC Updated

Always update:

- Phone number

- Address

- Email ID

Close Unused Accounts

If you no longer need an account, closing it may be better than leaving it inactive.

This also helps you manage finances more effectively, especially when planning for goals such as home loans and long-term financial planning.

Pros and Cons of Keeping an Old Bank Account

| Pros | Cons |

| Extra banking option | May become inactive |

| Emergency fund storage | Possible maintenance charges |

| Useful for old records | Risk of forgotten accounts |

| Backup account | Additional paperwork |

Common Mistakes Users Should Avoid

Many account holders unknowingly make mistakes that create problems later.

Ignoring Bank Messages

Do not ignore SMS or email notifications from your bank.

Forgetting Old Salary Accounts

Many people switch jobs and forget previous salary accounts.

Not Updating KYC

Outdated information can delay reactivation.

Keeping Too Many Accounts

Managing multiple accounts increases the risk of inactivity.

Assuming the Account Will Stay Active Forever

Even if money remains in the account, inactivity rules may still apply.

Additional Tips for Better Banking Management

To keep your finances organized:

- Review all bank accounts at least once every six months.

- Keep records of account numbers and branches.

- Link accounts to secure mobile banking apps.

- Monitor balances regularly.

- Understand your bank’s inactivity policy.

Learning more about banking and finance basics can help you avoid unnecessary issues and make better financial decisions.

If you plan to borrow in the future, understanding related topics such as personal loans or education loans can also improve financial planning.

Conclusion

Understanding what happens when bank account becomes inactive is important for every bank customer. An inactive account does not mean you lose your money, but it can restrict transactions and create inconvenience when you need access to funds.

Fortunately, reactivating an inactive account is usually simple if you update your documents and complete verification. By using your account occasionally, keeping KYC details updated, and monitoring bank notifications, you can avoid inactivity altogether.

Good banking habits help protect your money and keep your financial life running smoothly.

Frequently Asked Questions (FAQs)

1. How long does it take for a bank account to become inactive?

Many banks classify an account as inactive after 12 months without customer-initiated transactions. Policies may vary by bank.

2. Will I lose money if my bank account becomes inactive?

No. The money generally remains in your account, although certain charges may apply depending on bank policies.

3. Can I reactivate an inactive account online?

Some banks allow online reactivation, while others require visiting a branch with identity documents.

4. Is an inactive account the same as a dormant account?

No. Inactive accounts may later become dormant after a longer period of no activity.

5. Can an inactive account affect my credit score?

An inactive account itself usually does not affect your credit score. However, missed loan payments linked to that account could have an impact.

Read Also: Education Loan Interest During Study Period Explained

Leave a Reply