If you have ever missed an EMI payment, you may wonder whether it can affect your chances of getting a loan in the future. The simple answer is yes. Even one missed EMI can have an impact, depending on how late the payment is and how your lender reports it.

Many people miss an EMI because of unexpected expenses, a delayed salary, or simply forgetting the due date. While one mistake does not always mean your future loan application will be rejected, repeated missed payments can make lenders think you may have trouble repaying money on time.

Understanding can missed EMI affect future loan approval is important for anyone who has a loan or plans to borrow in the future. In this guide, you will learn how missed EMIs affect your credit score, why banks pay attention to your repayment history, and what you can do to improve your chances of loan approval.

Whether you are planning to apply for a personal loan, home loan, education loan, or another type of credit, maintaining a good repayment record can make the process much smoother.

What Is an EMI?

EMI stands for Equated Monthly Installment. It is the fixed amount you pay every month to repay a loan.

An EMI usually includes:

- A part of the loan amount (principal)

- Interest charged by the lender

People commonly pay EMIs for:

- Personal loans

- Home loans

- Education loans

- Car loans

- Consumer durable loans

Paying your EMI on or before the due date helps build a positive repayment history.

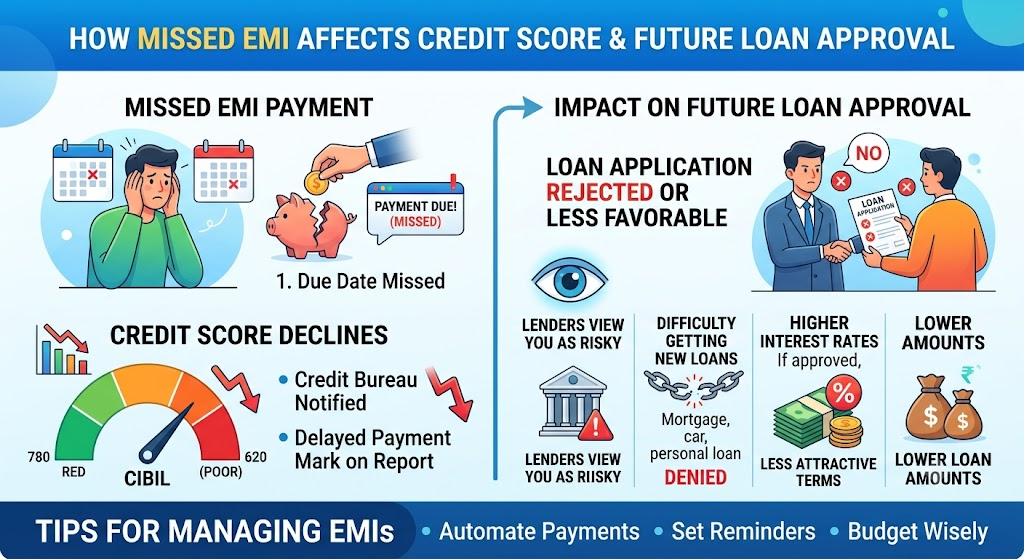

Can Missed EMI Affect Future Loan Approval?

Yes, can missed emi affect future loan approval is a common question because lenders closely review your repayment behavior before approving a new loan.

Whenever you apply for a loan, banks and financial institutions want to know whether you have repaid previous loans responsibly. Your EMI payment history gives them a clear picture of your financial discipline.

If you regularly miss EMIs, lenders may think:

- You struggle to manage your finances.

- There is a higher risk of delayed repayments.

- Approving another loan could be risky.

However, not every missed EMI has the same impact.

For example:

| Situation | Possible Impact |

|---|---|

| EMI paid a few days late | Usually limited if resolved quickly |

| EMI missed for several weeks | Can negatively affect your credit report |

| Multiple missed EMIs | Higher chance of loan rejection |

| Loan default | Serious impact on future borrowing |

The overall effect depends on factors such as the number of missed payments, the delay period, and your complete credit history.

Why Do Lenders Check EMI History?

Banks do not approve loans based only on your income. They also want to know whether you have managed previous loans responsibly.

Your EMI history helps lenders evaluate:

Your repayment discipline

Paying EMIs on time shows that you are responsible with borrowed money.

Your financial stability

Regular payments suggest that your income is sufficient to manage existing financial commitments.

Credit risk

Every lender wants to reduce the risk of loan defaults. A strong repayment history gives them greater confidence in approving your application.

How a Missed EMI Affects Your Credit Score

Your credit score is one of the first things lenders review when processing a loan application.

When an EMI remains unpaid and is reported to credit bureaus, your score may decrease.

A lower credit score can lead to:

- Lower chances of loan approval

- Higher interest rates

- Reduced loan amount

- Stricter eligibility requirements

On the other hand, paying EMIs on time consistently helps improve your credit profile over time.

If you are new to borrowing, you may also like reading our guide on how credit scores work and why they matter to better understand how lenders assess your financial health.

Does One Missed EMI Always Lead to Loan Rejection?

Fortunately, no.

A single missed EMI does not automatically mean your loan application will be rejected.

Lenders usually consider your overall financial profile.

For example, if:

- You have maintained a strong repayment record for several years,

- The missed payment was due to a temporary issue,

- The overdue amount was cleared quickly,

then the lender may still approve your application.

However, repeated delays tell a different story.

If someone misses EMIs frequently, lenders may believe there is a pattern of poor financial management.

Factors Banks Consider Before Approving a Loan

A missed EMI is only one part of the decision-making process.

Banks usually review several factors together.

| Factor | Why It Matters |

| Credit score | Indicates repayment behavior |

| EMI payment history | Shows financial discipline |

| Monthly income | Determines repayment capacity |

| Existing loans | Measures current debt burden |

| Employment stability | Reflects income consistency |

| Debt-to-income ratio | Shows ability to handle new debt |

Even if you have one delayed EMI, strong performance in other areas may improve your chances of approval.

Practical Example

Imagine two borrowers applying for the same personal loan.

Applicant A

- Pays every EMI on time.

- Has a stable income.

- Maintains a healthy credit score.

- Uses credit responsibly.

Applicant B

- Missed several EMIs during the past year.

- Frequently pays bills after the due date.

- Has a lower credit score.

- Already has multiple active loans.

Between the two applicants, the lender is generally more likely to approve Applicant A because they present a lower lending risk.

This example shows why consistent EMI payments play such an important role in future borrowing.

Pros and Cons of Maintaining Good EMI Payments

| Pros | Cons of Missing EMIs |

| Better credit score | Credit score may decrease |

| Higher loan approval chances | Future loans may become harder to obtain |

| Better interest rates | Possible late payment charges |

| Strong financial reputation | Reduced lender confidence |

| Easier access to credit | Lower borrowing limits in some cases |

Common Mistakes to Avoid After Missing an EMI

Missing one EMI does not always cause serious problems, but the actions you take afterward are important. Many borrowers make mistakes that worsen their financial situation.

Avoid these common mistakes:

1. Ignoring the Missed Payment

Some people believe the issue will resolve itself. In reality, unpaid EMIs may lead to late payment charges and can affect your credit history if they remain overdue.

2. Missing Multiple EMIs

One missed payment is usually less damaging than a pattern of late payments. Repeated delays make lenders less confident in your ability to repay future loans.

3. Applying for Multiple Loans Immediately

If your credit score has already been affected, applying for several loans or credit cards within a short period may create additional hard inquiries on your credit report. This can further reduce your chances of approval.

4. Not Contacting the Lender

If you are facing temporary financial difficulties, inform your lender as early as possible. Some lenders may offer solutions such as revised repayment schedules or temporary assistance, depending on your situation.

5. Forgetting Future EMI Due Dates

Many missed payments happen simply because borrowers forget the due date. Setting reminders or enabling auto-debit can help prevent this problem.

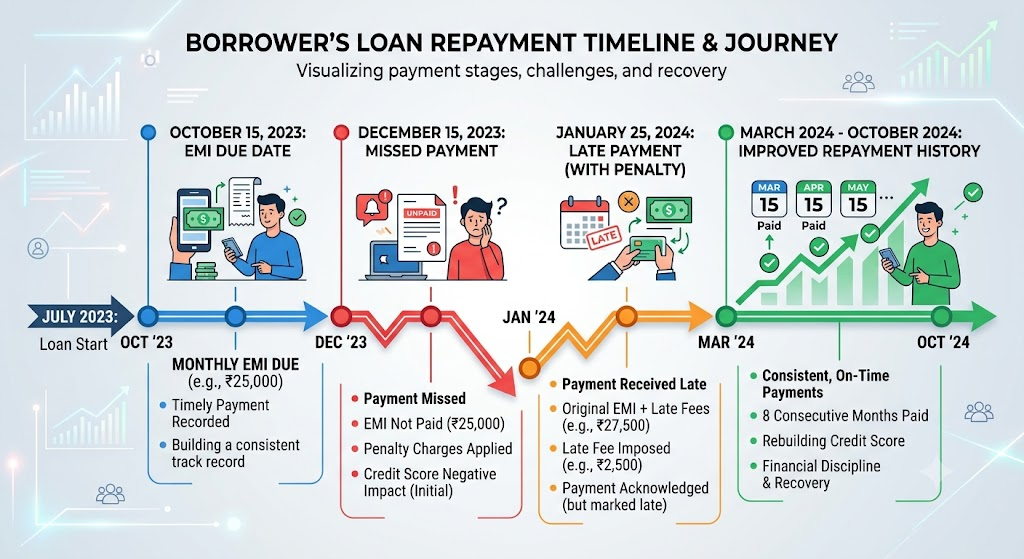

What Should You Do If You Miss an EMI?

If you have already missed an EMI, don’t panic. Acting quickly can help reduce the impact.

Pay the Outstanding Amount as Soon as Possible

The sooner you clear the overdue payment, the better. Delaying it further may increase penalties and negatively affect your repayment record.

Check Your Loan Account

Verify the outstanding amount, including any applicable late fees or interest.

Contact Your Lender

Explain your situation honestly if the delay was caused by unexpected circumstances. Good communication is always better than ignoring the issue.

Continue Paying Future EMIs on Time

One delayed payment becomes less significant if you maintain a consistent repayment record afterward.

Monitor Your Credit Report

Review your credit report periodically to ensure your loan information is accurate and to track your credit score over time.

Tips to Improve Your Chances of Future Loan Approval

Even if you have missed an EMI in the past, you can improve your financial profile.

Pay Every EMI Before the Due Date

Consistent on-time payments are one of the best ways to build trust with lenders.

Maintain a Good Credit Score

A healthy credit score reflects responsible borrowing habits and can improve your eligibility for future loans.

Avoid Taking Too Many Loans

Managing several loans at the same time may increase your financial burden. Borrow only when necessary.

Keep Your Debt Manageable

Try to maintain a reasonable debt-to-income ratio so lenders can see that you can comfortably repay additional borrowing.

Build a Stable Repayment History

Good financial habits over several months or years often matter more than one isolated mistake.

Quick Summary

| Question | Answer |

|---|---|

| Can a missed EMI affect future loan approval? | Yes, especially if payments are repeatedly missed. |

| Will one missed EMI always result in rejection? | No. Lenders usually consider your overall financial profile. |

| Does a missed EMI affect your credit score? | It can, particularly if the payment remains overdue and is reported. |

| Can your credit improve again? | Yes. Regular on-time payments over time can strengthen your credit profile. |

| Should you contact your lender after missing an EMI? | Yes. Early communication is generally recommended. |

Conclusion

To answer the question can missed emi affect future loan approval, the answer is yes—but the impact depends on your overall repayment history and financial habits.

One delayed EMI does not automatically mean your next loan application will be rejected. However, repeated missed payments can reduce your credit score, lower lender confidence, and make borrowing more difficult.

The good news is that you can improve your financial profile by paying future EMIs on time, managing your debts responsibly, and maintaining a healthy credit history.

Building good repayment habits not only increases your chances of loan approval but may also help you qualify for better interest rates and loan terms in the future.

Frequently Asked Questions

1. Can one missed EMI reduce my credit score?

Yes, it can if the missed payment is reported to credit bureaus. The impact depends on factors such as how late the payment is and your overall credit history.

2. How long does a missed EMI affect future loan approval?

The effect varies depending on your repayment behavior afterward. Maintaining timely payments over time can improve your credit profile.

3. Can I still get a loan after missing an EMI?

Yes. Many lenders evaluate your complete financial profile, including your income, repayment history, and current debt, rather than focusing on a single missed payment.

4. How can I avoid missing future EMIs?

You can set payment reminders, enable auto-debit from your bank account, and maintain enough balance before the EMI due date.

5. What should I do if I cannot pay my EMI on time?

Contact your lender as soon as possible. Depending on your circumstances and the lender’s policies, they may discuss available repayment options.

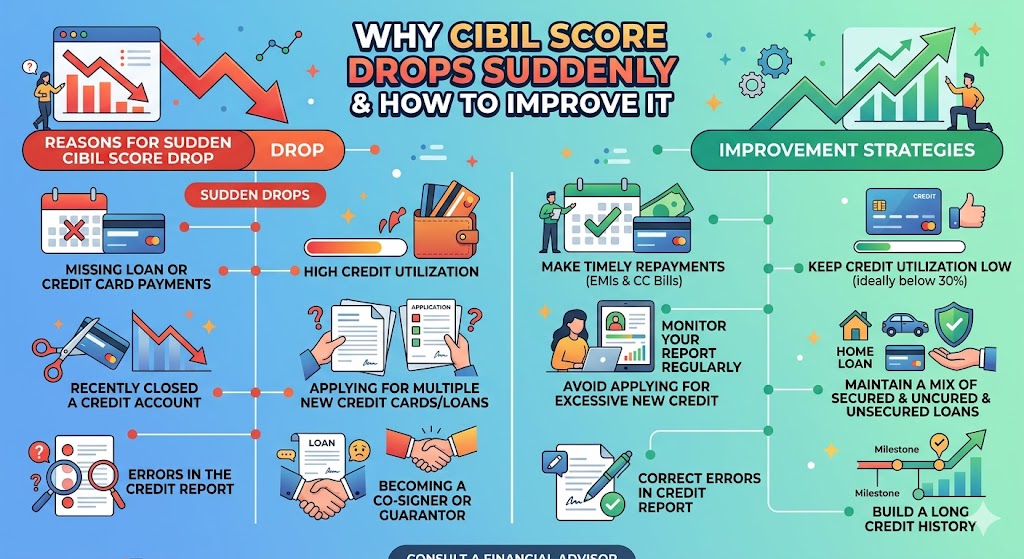

Read Also: Why Does Your CIBIL Score Drop Suddenly?

Leave a Reply