A good CIBIL score plays an important role when you apply for a loan or credit card. Most lenders use your credit score to understand how responsibly you manage borrowed money. Therefore, seeing a sudden drop in your CIBIL score can be surprising and stressful.

Many people regularly check their credit score and notice that it has fallen even though they believe they have done nothing wrong. In reality, several factors can cause a sudden decline in your score. Some reasons are minor and temporary, while others may require immediate attention.

In this guide, we will explain why CIBIL score drops suddenly, the most common causes behind it, and what you can do to improve your score over time.

What Is a CIBIL Score?

A CIBIL score is a three-digit number that reflects your creditworthiness. It usually ranges from 300 to 900.

Generally:

| CIBIL Score Range | Meaning |

|---|---|

| 750 – 900 | Excellent |

| 700 – 749 | Good |

| 650 – 699 | Fair |

| 550 – 649 | Poor |

| Below 550 | Very Poor |

A higher score can improve your chances of getting approved for:

- Personal loans

- Home loans

- Education loans

- Credit cards

- Vehicle loans

Lenders often prefer borrowers with a score above 750.

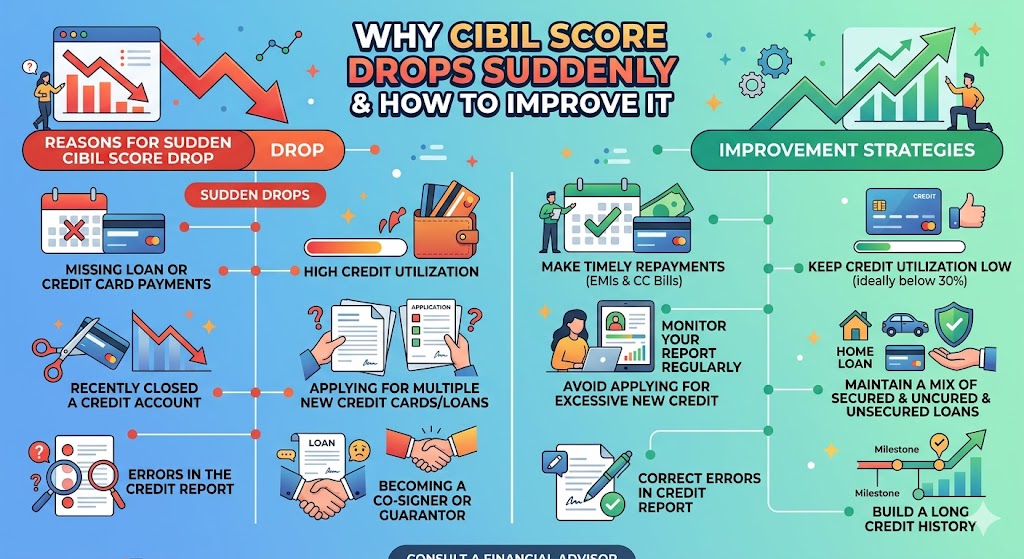

Why CIBIL Score Drops Suddenly

If you are wondering why CIBIL score drops suddenly, the answer usually lies in recent changes to your credit behavior or credit report.

Even one missed payment or a sudden increase in credit card usage can affect your score. Sometimes, errors in your credit report may also cause unexpected drops.

Let’s look at the most common reasons in detail.

Common Reasons for a Sudden Credit Score Drop

1. Missing an EMI or Credit Card Payment

Payment history is one of the biggest factors affecting your CIBIL score.

If you miss:

- A loan EMI

- A credit card bill

- A minimum payment due

Your lender may report the delay to the credit bureau.

Even a single missed payment can negatively impact your score.

Example

Suppose your score is 780 and you forget to pay your credit card bill for a month. Your score may drop significantly depending on your overall credit profile.

2. High Credit Card Utilization

Credit utilization refers to how much of your available credit limit you are using.

For example:

- Credit limit: ₹1,00,000

- Amount used: ₹80,000

Your utilization ratio is 80%.

Most experts recommend keeping utilization below 30%.

High utilization may indicate financial stress, which can lower your credit score.

3. Applying for Multiple Loans or Credit Cards

Every time you apply for a loan or credit card, the lender performs a hard inquiry on your credit report.

One inquiry may have a small impact.

However, multiple applications within a short period can make lenders think that you urgently need credit.

As a result, your score may decrease.

4. Closing an Old Credit Card

Many people believe closing unused credit cards will improve their score.

In some cases, the opposite happens.

Older credit accounts contribute to your credit history length. When you close a long-standing credit card:

- Average account age may reduce

- Available credit limit may decrease

- Credit utilization ratio may increase

These factors can negatively affect your score.

5. Errors in Your Credit Report

Sometimes the issue is not your fault.

Your credit report may contain:

- Incorrect loan information

- Wrong payment records

- Duplicate accounts

- Loans belonging to someone else

Such errors can lower your score unexpectedly.

This is why reviewing your credit report regularly is important.

6. Loan Settlement Instead of Full Repayment

Some borrowers choose loan settlement during financial difficulties.

While settlement can reduce immediate financial pressure, it may hurt your credit score.

A settled loan tells future lenders that the borrower did not repay the entire amount according to the original agreement.

This can remain on your credit report for years.

7. Becoming a Loan Guarantor

Many people do not realize that being a guarantor carries financial responsibility.

If the primary borrower:

- Misses payments

- Defaults on the loan

Your credit score may also be affected.

Before becoming a guarantor, understand the risks involved.

8. Increase in Outstanding Debt

Taking on too much debt can impact your score.

For example:

- Personal loan

- Credit card debt

- Consumer durable loan

If your total debt increases significantly within a short period, lenders may view you as a higher-risk borrower.

9. Inactive Credit History

Having no recent credit activity can sometimes lead to small score fluctuations.

Credit bureaus prefer to see active and responsible credit behavior.

If you stop using all credit products for a long period, your score may not improve as expected.

10. Recent Loan Default Reporting

Sometimes lenders report delayed payments after updating their records.

You may notice a score drop even if the payment issue happened several weeks earlier.

This delayed reporting often surprises borrowers.

How Much Can a CIBIL Score Fall?

The impact varies from person to person.

Factors include:

- Existing score

- Credit history length

- Number of active loans

- Severity of the issue

For example:

| Situation | Possible Impact |

|---|---|

| One hard inquiry | Small drop |

| High credit utilization | Moderate drop |

| Missed EMI payment | Significant drop |

| Loan default | Major drop |

| Credit report error | Varies |

Someone with a high score may notice a larger drop after a serious negative event because they have more points to lose.

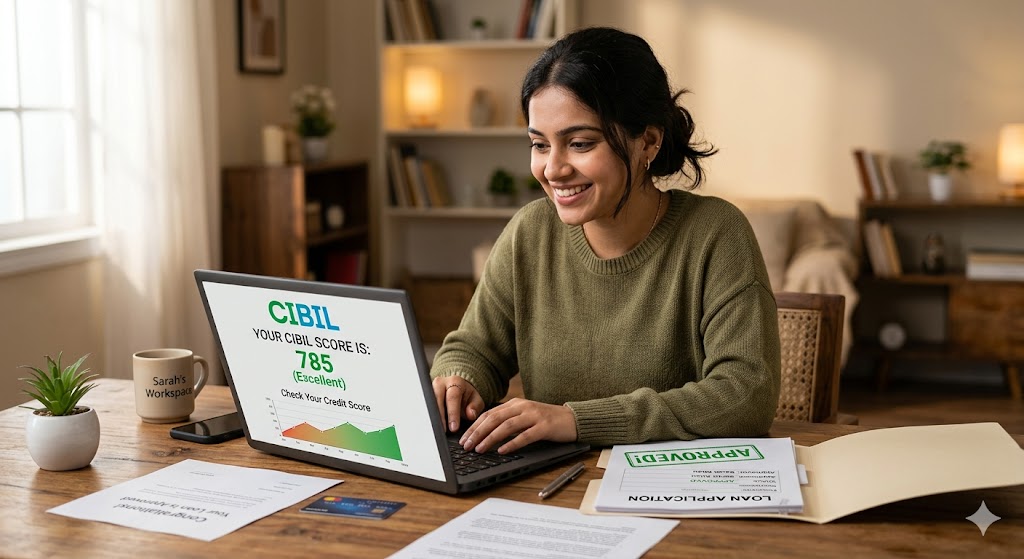

Practical Example

Consider Rahul, who has a CIBIL score of 785.

In one month he:

- Applied for two credit cards

- Used 85% of his available credit limit

- Missed one credit card payment

A month later, his score dropped noticeably.

The decline happened because multiple risk factors occurred at the same time.

After paying dues on time and reducing credit utilization, his score gradually started recovering over the following months.

Pros and Cons of Credit Monitoring

Pros

- Helps identify errors quickly

- Detects fraudulent activity

- Tracks score improvement

- Improves financial planning

- Helps prepare for loan applications

Cons

- Minor score changes may cause unnecessary worry

- Some paid monitoring services may be expensive

- Frequent checking does not instantly improve the score

Common Mistakes to Avoid

Many borrowers unknowingly damage their credit score.

Avoid these mistakes:

- Missing payment due dates

- Using most of your credit limit

- Applying for many loans at once

- Ignoring credit report errors

- Settling loans without understanding consequences

- Closing old credit cards unnecessarily

- Becoming a guarantor without evaluating risks

Tips to Improve Your CIBIL Score

If your score has dropped, don’t panic. Recovery is possible with consistent habits.

Pay Bills on Time

Set reminders or use auto-pay features to avoid missed payments.

Reduce Credit Card Usage

Try to keep utilization below 30% of the available limit.

Check Your Credit Report Regularly

Look for inaccuracies and dispute any incorrect information.

Avoid Multiple Loan Applications

Apply only when necessary.

Maintain Older Credit Accounts

Older accounts help build a stronger credit history.

Repay Outstanding Debt

Focus on reducing existing debt before taking new loans.

Build a Healthy Credit Mix

Having a combination of secured and unsecured credit can help improve your credit profile over time.

Conclusion

Understanding why CIBIL score drops suddenly is important for maintaining good financial health. In most cases, the reasons include missed payments, high credit card usage, multiple loan applications, increased debt, or errors in your credit report.

The good news is that a lower score is not permanent. By paying bills on time, keeping credit utilization low, monitoring your credit report, and avoiding unnecessary loan applications, you can gradually rebuild your credit profile.

A strong CIBIL score not only improves your chances of loan approval but may also help you secure better interest rates in the future.

Frequently Asked Questions (FAQs)

1. Can my CIBIL score drop even if I paid all bills on time?

Yes. High credit utilization, multiple loan applications, account closures, or reporting errors can still cause a score decrease.

2. How often is the CIBIL score updated?

Most lenders report data monthly, so your score may change after new information is added to your credit report.

3. How long does it take to recover a dropped CIBIL score?

It depends on the reason. Minor drops may recover within a few months, while serious issues like defaults can take much longer.

4. Does checking my own CIBIL score reduce it?

No. Checking your own score is considered a soft inquiry and does not affect your credit score.

5. What is considered a good CIBIL score for a loan?

Generally, a score of 750 or above is considered good and may improve your chances of loan approval.

Read Also: How to Improve Your CIBIL Score for Loan Approval

Leave a Reply