Education loans help students achieve their academic goals when personal savings are not enough. They make higher education more accessible and allow students to focus on learning instead of worrying about immediate expenses.

However, many borrowers and their families often wonder: what happens if education loan is not repaid?

Missing a few payments may seem like a small issue at first. But over time, unpaid education loans can create serious financial problems. Your credit score may drop, penalties may increase the loan amount, and lenders may start recovery actions.

The good news is that borrowers usually have several options before the situation becomes severe. Understanding the consequences early can help you take the right steps and avoid long-term financial difficulties.

What Is an Education Loan?

An education loan is a type of financial assistance provided by banks and financial institutions to help students pay for:

- Tuition fees

- Hostel expenses

- Books and study materials

- Examination fees

- Travel expenses for overseas education

- Other educational costs

Most education loans include a moratorium period, which means repayment usually begins after the course is completed and a specified waiting period ends.

What Happens If Education Loan Is Not Repaid?

When an education loan is not repaid on time, lenders may take several actions depending on the delay period and loan agreement.

Some common consequences include:

| Consequence | Impact |

|---|---|

| Late payment charges | Increases total loan cost |

| Credit score damage | Makes future borrowing difficult |

| Loan default status | Negative record with credit bureaus |

| Recovery actions | Calls, notices, and follow-ups |

| Legal proceedings | Possible in severe cases |

| Co-applicant liability | Parent or guardian may become responsible |

The longer the loan remains unpaid, the more serious the consequences become.

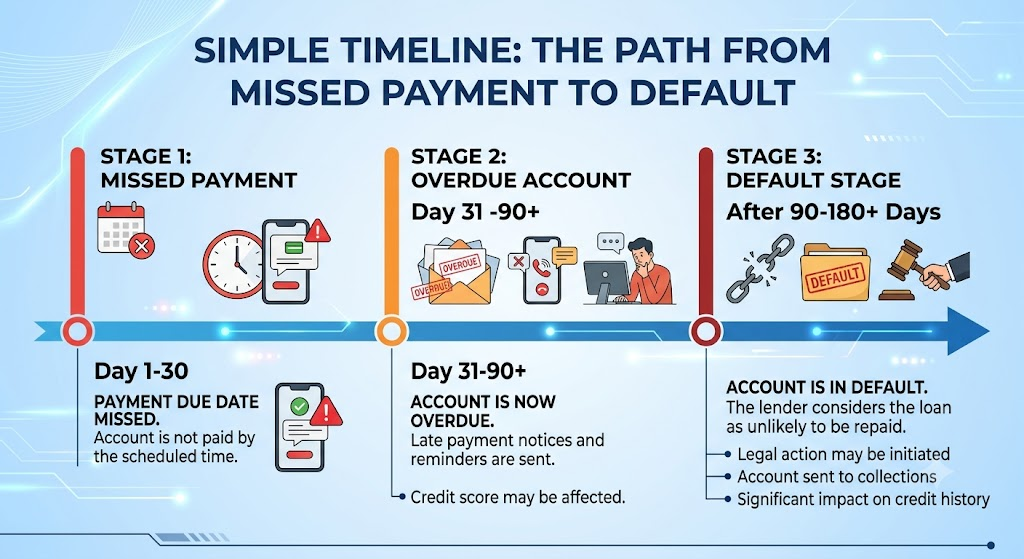

Stages of Education Loan Default

Understanding how default develops can help borrowers act before the situation worsens.

1. Missed Payment

The process usually begins when a borrower misses a monthly installment.

Initially, the lender may:

- Send reminders

- Make phone calls

- Send emails or SMS notifications

At this stage, resolving the issue is often simple.

2. Repeated Missed Payments

If payments continue to be missed, the lender may classify the account as overdue.

Additional charges may start accumulating.

3. Loan Default

After prolonged non-payment, the lender may mark the loan as defaulted according to banking regulations and internal policies.

At this stage:

- Credit reports are affected

- Recovery efforts increase

- Future loan approvals become harder

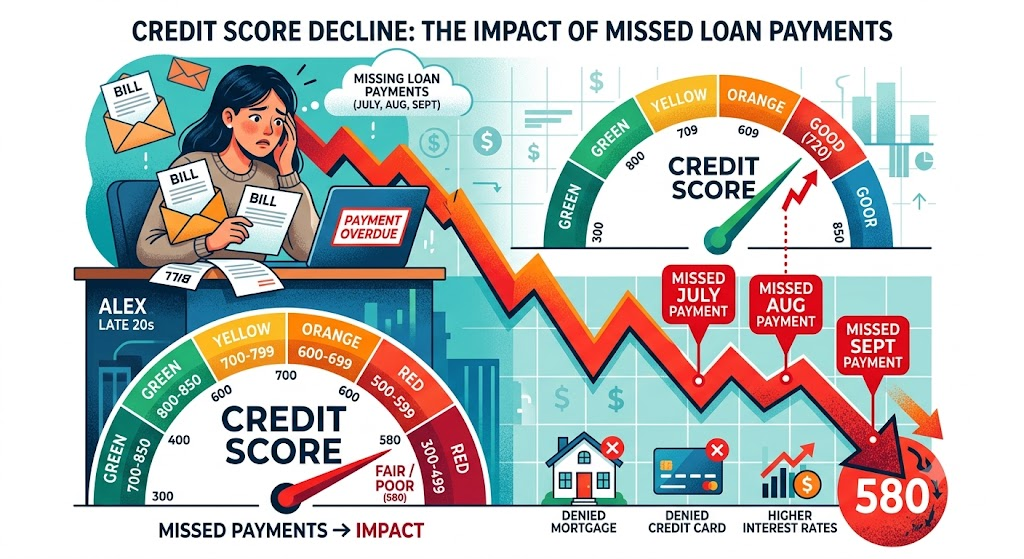

Impact on Credit Score

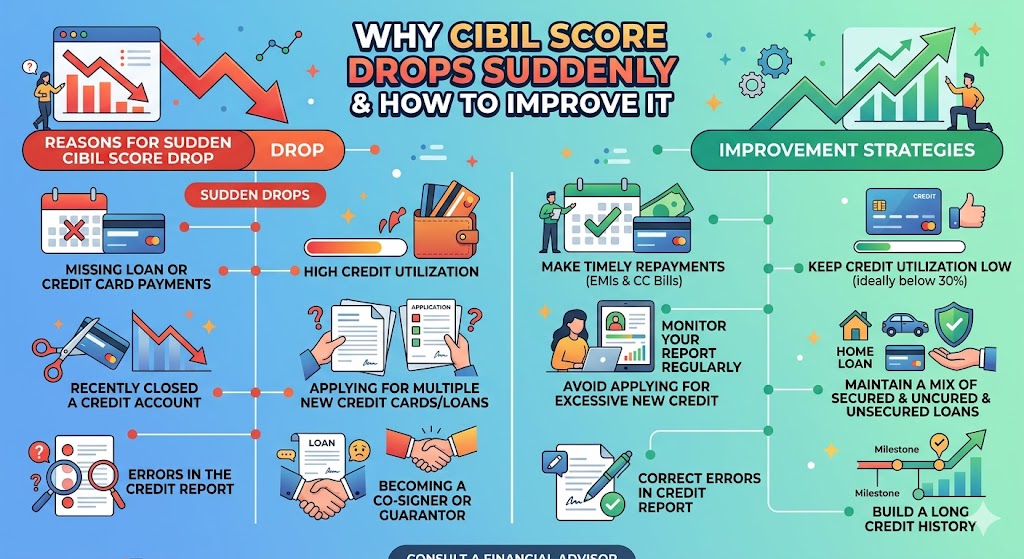

One of the biggest consequences of not repaying an education loan is damage to your credit score.

A credit score helps lenders evaluate your ability to repay debt.

When payments are missed:

- Negative records appear in your credit history

- Future loans may become difficult to obtain

- Credit card approvals may be affected

- Borrowing costs may increase

For example, if you plan to apply for a home loan after a few years, a poor repayment record can reduce your chances of approval.

If you want to understand this topic further, you can also create an internal link to your website’s article about credit score improvement and loan eligibility.

Penalties and Additional Charges

Education loans often include clauses related to late payments.

These may include:

- Late payment penalties

- Additional interest charges

- Collection costs

- Administrative fees

Over time, these extra costs can significantly increase the amount owed.

Example

Suppose a borrower misses several installments. The unpaid amount continues to attract interest while penalties are added.

As a result, the outstanding balance may become much larger than expected.

Can the Lender Take Legal Action?

Yes, lenders can take legal action in serious cases of prolonged non-payment.

However, legal action is usually considered after several attempts to recover the dues through communication and settlement efforts.

Possible actions may include:

- Sending legal notices

- Initiating recovery proceedings

- Filing cases as permitted under applicable laws

The exact process depends on:

- Loan amount

- Loan agreement terms

- Applicable regulations

- Borrower’s repayment history

Because legal processes can be stressful and expensive, borrowers should communicate with lenders as soon as financial difficulties arise.

What Happens to the Co-Applicant?

Most education loans require a co-applicant.

This is usually:

- A parent

- A guardian

- A spouse (in some cases)

Many borrowers do not realize that the co-applicant shares responsibility for repayment.

If the borrower fails to repay:

- Recovery notices may be sent to the co-applicant

- The co-applicant’s credit profile may be affected

- The lender may seek repayment from both parties

This is why families should carefully plan repayment before taking an education loan.

Situations Where Repayment Becomes Difficult

Borrowers may struggle to repay loans for many genuine reasons.

Common examples include:

Unemployment

After graduation, finding a job may take longer than expected.

Low Starting Salary

Some graduates secure jobs but earn less than anticipated.

Medical Emergencies

Unexpected health issues can affect income and savings.

Career Changes

Switching industries or preparing for competitive exams may delay earnings.

Economic Conditions

Market downturns can affect employment opportunities.

In such situations, ignoring the lender is usually the worst option.

Options Available for Borrowers

If you are facing repayment difficulties, several solutions may be available.

Loan Restructuring

Some lenders may offer revised repayment terms.

This can help reduce monthly installment pressure.

Temporary Relief Programs

Depending on lender policies and regulations, temporary repayment support may be available.

Extended Repayment Tenure

Increasing the repayment period may lower monthly payments.

Partial Payments

Even partial payments may demonstrate repayment intent and help avoid deeper default issues.

Direct Communication With the Lender

The most important step is contacting the lender early.

Many repayment problems can be addressed through discussion before they become serious.

Common Mistakes to Avoid

Borrowers often make mistakes that worsen their situation.

Avoid these common errors:

- Ignoring bank calls and notices

- Assuming the problem will disappear

- Missing multiple payments without informing the lender

- Not checking loan statements

- Depending entirely on future income expectations

- Borrowing additional money without a repayment plan

Being proactive can prevent long-term financial damage.

Helpful Tips for Managing Education Loan Repayment

Create a Monthly Budget

Track income and expenses carefully.

Build an Emergency Fund

Savings can help during temporary financial difficulties.

Start Repayment Planning Early

Even before graduation, understand future repayment obligations.

Monitor Your Credit Report

Regular monitoring helps identify problems quickly.

Avoid Unnecessary Debt

Taking multiple loans simultaneously may increase financial pressure.

You may also internally link to a future article about personal loan vs education loan differences for readers comparing borrowing options.

Another useful internal linking opportunity is a guide on banking and finance basics for first-time borrowers.

Pros and Cons of Education Loans

| Pros | Cons |

| Helps fund higher education | Creates repayment obligation |

| Provides access to quality institutions | Interest increases overall cost |

| Allows students to invest in future careers | Missed payments affect credit score |

| May offer flexible repayment options | Financial stress if income is delayed |

| Reduces immediate financial burden | Default can lead to recovery action |

Conclusion

Understanding what happens if education loan is not repaid is important for every student and family considering educational financing.

Failure to repay an education loan can lead to penalties, credit score damage, recovery efforts, and potential legal consequences. In many cases, the co-applicant may also be affected.

Fortunately, borrowers facing financial difficulties often have options such as restructuring, revised repayment plans, or direct discussions with the lender. Acting early is usually the best way to prevent a temporary challenge from becoming a long-term financial problem.

Responsible borrowing and timely repayment can help protect your financial future while allowing you to benefit from the opportunities that education loans provide.

Read Also: Education Loan Repayment Process Explained Simply

Frequently Asked Questions

1. Can I go to jail for not repaying an education loan?

Generally, loan non-payment is treated as a financial matter rather than a criminal offense. However, lenders may pursue recovery and legal procedures according to applicable laws.

2. Does an unpaid education loan affect my credit score?

Yes. Missed payments and loan defaults can negatively affect your credit score and future borrowing ability.

3. Can the bank recover the loan from my parents?

If your parents are co-applicants or guarantors, they may also be responsible for repayment obligations.

4. What should I do if I cannot repay my education loan?

Contact your lender immediately. Options such as restructuring or modified repayment plans may be available.

5. Can I get another loan after defaulting on an education loan?

It may become more difficult because lenders often review your credit history before approving new loans.

Leave a Reply