Higher education is becoming more expensive every year. Many students and parents worry about arranging money for college fees, hostel expenses, books, and other education costs. One common question students ask is: Can Students Get Education Loans Without Collateral?

The good news is that many banks and financial institutions in India offer education loans without asking for collateral security. This can help students who do not own property or other valuable assets.

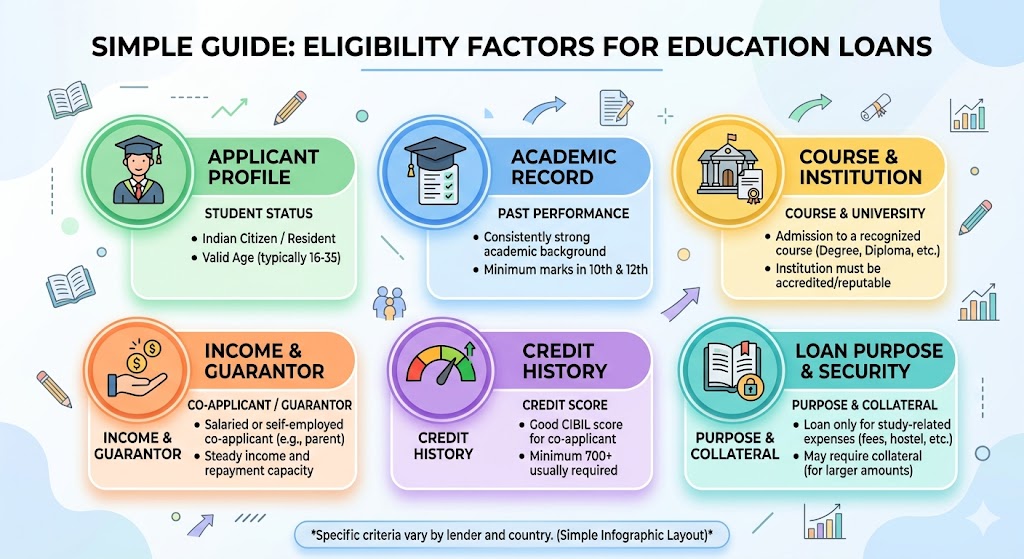

However, getting a collateral-free education loan depends on several factors like the loan amount, college reputation, student profile, co-applicant income, and credit history.

In this guide, you will learn how these loans work, who can apply, eligibility requirements, advantages, disadvantages, and important mistakes to avoid before applying.

What Is a Collateral-Free Education Loan?

A collateral-free education loan is a student loan that does not require security such as:

- House property

- Fixed deposits

- Land

- Gold

- Investments

In simple words, the bank gives the loan based on the student’s academic profile and the financial background of the co-applicant, usually parents or guardians.

These loans are commonly available for:

- Undergraduate courses

- Postgraduate courses

- Professional courses

- Study abroad programs

- Technical and management courses

Can Students Get Education Loans Without Collateral?

Yes, students can get education loans without collateral in many cases.

Most banks and NBFCs offer unsecured education loans for deserving students. Usually, smaller loan amounts are easier to get without security. Some lenders also provide larger collateral-free loans for students studying at top universities in India or abroad.

The approval mainly depends on:

| Factor | Importance |

|---|---|

| Academic performance | Very important |

| College or university ranking | Important |

| Course type | Important |

| Co-applicant income | Very important |

| Credit score of co-applicant | Important |

| Future earning potential | Considered by lenders |

For example, a student getting admission into a well-known engineering or medical college may have better chances of receiving a collateral-free loan compared to a student applying for an unknown course or institution.

Eligibility Criteria for Education Loans Without Collateral

Different lenders have different rules, but most require the following conditions.

Student Must Be an Indian Citizen

Most banks provide education loans only to Indian citizens. Some lenders may also support NRI students under special conditions.

Confirmed Admission Is Required

The student must have secured admission in a recognized college or university.

This can include:

- Government colleges

- Private universities

- Foreign universities

- Technical institutes

- Professional education institutions

Co-Applicant Is Usually Mandatory

A co-applicant is normally required for unsecured education loans.

The co-applicant can be:

- Parent

- Guardian

- Spouse in some cases

The bank checks the co-applicant’s:

- Income stability

- Existing loans

- Credit score

- Repayment history

If you want to understand how credit history affects loans, you can also read your internal guide on credit scores and loan eligibility.

Good Academic Record Helps

Students with strong academic performance may receive better loan offers.

Banks may look at:

- School marks

- Entrance exam scores

- Graduation marks

- Career potential

Documents Required

Below are the common documents needed when applying for a collateral-free education loan.

| Document Type | Examples |

|---|---|

| Identity Proof | Aadhaar Card, PAN Card |

| Address Proof | Utility bill, Passport |

| Academic Records | Mark sheets, certificates |

| Admission Proof | Offer letter from college |

| Fee Structure | Official fee document |

| Income Proof of Co-Applicant | Salary slips, ITR |

| Bank Statements | Last 6 months |

| Passport Photos | Student and co-applicant |

Some lenders may ask for additional documents depending on the loan amount and course.

Loan Amount Available Without Collateral

The maximum loan amount without collateral varies from lender to lender.

Here is a general idea:

| Type of Course | Typical Loan Amount Without Collateral |

|---|---|

| Study in India | Up to ₹7.5 lakh commonly |

| Top Indian Institutes | Higher amounts possible |

| Study Abroad | ₹20 lakh or more in selected cases |

Some private lenders and NBFCs may offer larger unsecured loans for top-ranked international universities.

However, higher loan amounts usually require:

- Strong co-applicant income

- Excellent academic profile

- High future earning potential

Interest Rates and Repayment

Interest rates on collateral-free education loans are generally slightly higher than secured loans because the bank takes more risk.

Interest Rate Factors

The interest rate depends on:

- Student profile

- University ranking

- Loan amount

- Co-applicant credit history

- Type of lender

Moratorium Period

Most education loans include a moratorium period. This means repayment usually starts after:

- Course completion, plus

- 6 to 12 months

This gives students time to find a job before beginning EMI payments.

Loan Repayment Tenure

Repayment tenure may range from:

- 5 years

- 10 years

- Up to 15 years in some cases

Longer tenure reduces monthly EMI but increases total interest paid.

Students comparing loan repayment options may also find your banking and finance guides useful for understanding EMI calculations and budgeting.

Pros and Cons of Collateral-Free Education Loans

Advantages

No Need for Property or Assets

Families without property can still arrange funds for education.

Faster Processing

Documentation may be simpler compared to secured loans.

Supports Higher Education Dreams

Students can pursue professional courses without immediate financial burden.

Flexible Repayment Options

Most lenders provide repayment after course completion.

Disadvantages

Higher Interest Rates

Unsecured loans often cost more than secured loans.

Strict Eligibility Checks

Banks carefully evaluate academic and financial profiles.

Lower Loan Limits

Some lenders may restrict the maximum loan amount without collateral.

Co-Applicant Responsibility

If the student cannot repay, the co-applicant becomes responsible for repayment.

Common Reasons for Loan Rejection

Many students get rejected because of avoidable issues.

Poor Credit Score of Co-Applicant

Banks check repayment history carefully.

Weak Academic Background

Low marks or inconsistent performance may reduce approval chances.

Unrecognized College or Course

Some lenders only support approved institutions.

Low Family Income

The bank must feel confident about future repayment ability.

Incomplete Documentation

Missing documents can delay or reject applications.

Tips to Improve Approval Chances

Apply Early

Do not wait until the last minute after receiving admission confirmation.

Maintain Good Academic Scores

Strong marks improve lender confidence.

Choose Recognized Institutions

Well-known colleges improve approval chances.

Improve Co-Applicant Credit Score

Clear existing dues and avoid missed EMIs before applying.

Compare Multiple Lenders

Interest rates and loan conditions differ across banks and NBFCs.

Students sometimes compare education loans with personal loans for education expenses. However, education loans usually offer lower interest rates and better repayment flexibility than personal loans.

Read Also: Documents Required for First-Time Home Loan Applicants

Common Mistakes Students Should Avoid

Borrowing More Than Necessary

Only take the amount actually needed for education expenses.

Ignoring Loan Terms

Always read:

- Interest rates

- Processing fees

- Repayment conditions

- Penalties

Not Comparing Loan Offers

Different lenders may provide better benefits for the same student profile.

Missing EMI Payments Later

Late payments can damage both student and co-applicant credit scores.

Choosing Unknown Institutions

Banks may hesitate to fund courses with poor career opportunities.

Conclusion

So, Can Students Get Education Loans Without Collateral? The answer is yes. Many banks and financial institutions now provide collateral-free education loans for eligible students.

These loans can help students continue their higher education even if their families do not own property or valuable assets. However, approval depends on academic performance, the college chosen, co-applicant income, and overall financial stability.

Before applying, students should compare lenders carefully, understand repayment terms, and borrow responsibly. A well-planned education loan can support long-term career growth without creating unnecessary financial stress.

FAQs

1. Can I get an education loan without collateral for studying abroad?

Yes, some banks and NBFCs provide collateral-free education loans for studying abroad, especially for top-ranked universities.

2. Is a co-applicant mandatory for education loans without collateral?

In most cases, yes. Parents or guardians usually act as co-applicants.

3. What is the maximum education loan available without collateral?

The amount varies by lender. Some banks provide up to ₹7.5 lakh commonly, while others may offer higher amounts for top institutions.

4. Does the co-applicant’s credit score matter?

Yes, a good credit score improves the chances of approval and may help in getting better interest rates.

5. Can unemployed students apply for education loans?

Yes. Since students usually do not have income, lenders mainly evaluate the co-applicant’s financial condition and the student’s academic profile.

Also See: How to Check Personal Loan Eligibility Before Applying