Applying for a personal loan without understanding your eligibility can lead to rejection, lower credit scores, and unnecessary stress. That is why it is important to check personal loan eligibility before submitting an application.

Many beginners think banks approve loans only based on salary. However, lenders also check your credit history, monthly expenses, employment stability, existing loans, and repayment ability.

The good news is that you can check most eligibility factors yourself before applying. This helps you choose the right lender and improve your chances of approval.

In this guide, you will learn how to check personal loan eligibility before applying in simple language. Whether you are applying for your first loan or trying to improve your approval chances, this article will help you make better financial decisions.

What Is Personal Loan Eligibility?

Personal loan eligibility means whether you qualify for a loan based on the lender’s requirements.

Banks and financial institutions use eligibility rules to decide:

- Whether you can repay the loan

- How much loan amount you can get

- What interest rate you may receive

- How long your repayment period can be

Each lender has slightly different rules. However, most banks check similar financial factors before approving a loan.

Why Checking Eligibility Is Important

Checking eligibility before applying offers several benefits.

It Helps Avoid Loan Rejections

Multiple rejected loan applications can negatively affect your credit profile. Therefore, it is better to apply only when you meet the basic requirements.

It Saves Time

You can quickly understand which lenders match your financial situation.

It Helps You Plan Better

When you know your estimated eligible amount, you can plan your budget and EMI comfortably.

It Protects Your Credit Score

Too many loan applications within a short period may lower your credit score.

If you want to understand how credit ratings work, you can also read related articles about improving your credit score and maintaining healthy banking habits.

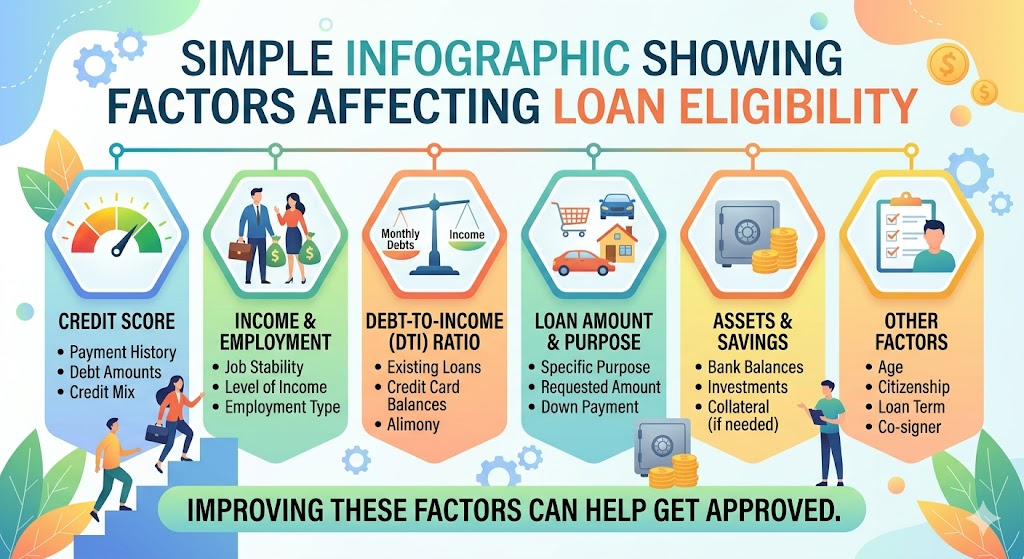

Main Factors That Affect Personal Loan Eligibility

Before learning how to check personal loan eligibility before applying, you should understand the factors banks usually check.

How to Check Personal Loan Eligibility Before Applying

1. Check Your Monthly Income

Your income is one of the most important factors.

Lenders want to see whether you earn enough money to repay the loan on time.

Generally, salaried employees with stable monthly income have higher approval chances.

Banks usually prefer applicants who:

- Have regular salary income

- Receive salary in a bank account

- Meet the lender’s minimum income requirement

For example:

| Monthly Income | Possible Loan Eligibility |

|---|---|

| ₹20,000 | Lower loan amount |

| ₹40,000 | Medium loan amount |

| ₹80,000+ | Higher loan amount |

The actual loan amount depends on other factors too.

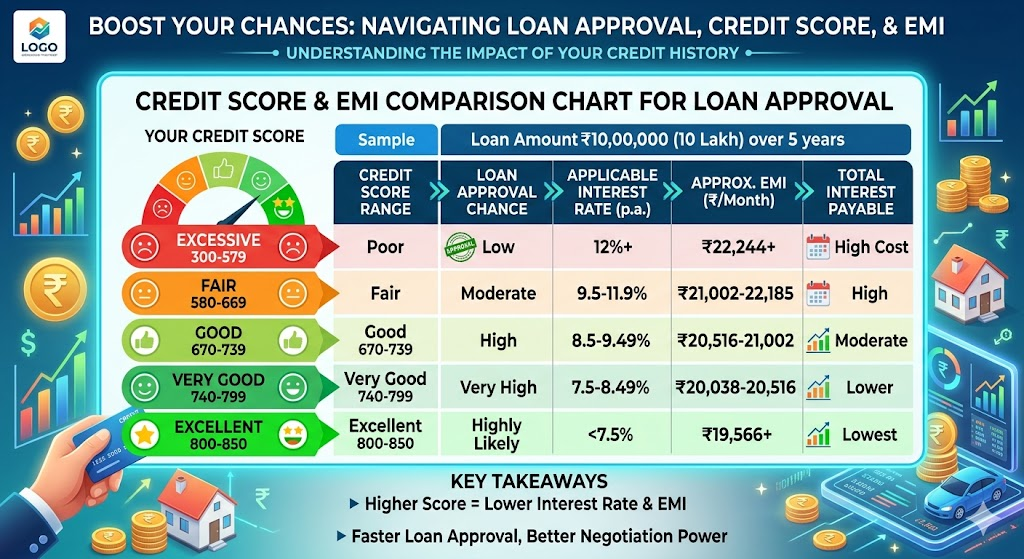

2. Check Your Credit Score

A credit score reflects your repayment history.

Most lenders prefer a credit score of:

- 750 or above for better approval chances

- 700+ for moderate approval possibility

A low score may lead to:

- Higher interest rates

- Lower loan amount

- Loan rejection

You can check your credit score online through authorized credit bureaus or banking apps.

If your score is low, consider improving it before applying. Reading guides related to credit score improvement can help beginners understand the process better.

3. Calculate Your Existing EMI Burden

Banks also check how much of your income already goes toward existing EMIs.

This is called the debt-to-income ratio.

For example:

| Monthly Income | Existing EMIs | Risk Level |

|---|---|---|

| ₹50,000 | ₹5,000 | Low |

| ₹50,000 | ₹25,000 | High |

If most of your income already goes toward loan payments, lenders may hesitate to approve another loan.

Experts generally recommend keeping total EMIs below 40% to 50% of monthly income.

4. Verify Employment Stability

Job stability matters a lot.

Lenders usually prefer:

- Salaried employees with stable jobs

- Applicants working for at least 6–12 months

- Professionals with regular income

Frequent job changes may reduce approval chances.

Self-employed individuals may need:

- Income tax returns

- Business proof

- Bank statements

5. Check Your Age Eligibility

Most banks have age requirements.

Generally:

- Minimum age: 21 years

- Maximum age: 58–65 years

Different lenders may have different policies.

6. Review Your Bank Statements

Banks often check your recent bank transactions.

They look for:

- Regular salary deposits

- Good account balance

- Responsible spending habits

- No frequent cheque bounces

Poor banking behavior may affect approval.

If you want to learn more about managing bank accounts properly, reading beginner-friendly banking and finance articles can be useful.

7. Use an Online Loan Eligibility Calculator

Many banks provide eligibility calculators on their websites.

These tools estimate:

- Loan amount

- EMI

- Interest cost

- Repayment period

Usually, you need to enter:

- Monthly income

- Existing EMIs

- Loan tenure

- Employment type

These calculators provide estimates, not guaranteed approval.

Common Reasons Why Loans Get Rejected

Understanding rejection reasons helps you prepare better.

Low Credit Score

Missed payments and credit card defaults can reduce approval chances.

Insufficient Income

If your income does not meet the lender’s minimum requirement, your application may get rejected.

Too Many Existing Loans

High EMI burden increases financial risk for lenders.

Frequent Loan Applications

Applying to many lenders at once may negatively affect your credit profile.

Unstable Employment

Frequent job changes may create repayment concerns.

Incorrect Documents

Errors in documents or incomplete information can delay or reject applications.

Tips to Improve Your Loan Eligibility

If your eligibility is currently weak, do not worry. You can improve it over time.

Pay Existing EMIs on Time

Timely payments improve your credit profile gradually.

Reduce Credit Card Debt

Lower outstanding balances improve repayment capacity.

Avoid Multiple Loan Applications

Apply carefully after checking lender requirements.

Maintain Stable Employment

Longer work history often improves lender confidence.

Choose a Suitable Loan Amount

Applying for a smaller amount may improve approval chances.

Add a Co-Applicant if Needed

Some lenders may consider combined income for better eligibility.

Pros and Cons of Checking Eligibility Early

| Pros | Cons |

|---|---|

| Helps avoid rejection | Estimates may not be exact |

| Protects credit score | Different lenders have different rules |

| Saves time | Some checks may require personal details |

| Helps compare lenders | Approval is never guaranteed |

Common Mistakes to Avoid

Many beginners make avoidable mistakes during the loan process.

Ignoring Credit Score

Some people apply without checking their score first.

Applying for Very High Loan Amounts

Requesting unrealistic loan amounts may reduce approval chances.

Submitting Multiple Applications Together

Too many applications can make lenders cautious.

Hiding Existing Loans

Always provide accurate financial information.

Not Reading Loan Terms

Understand interest rates, processing fees, and repayment conditions before applying.

Practical Example of Checking Eligibility

Suppose Rahul earns ₹45,000 per month.

His current EMIs:

- Bike loan EMI: ₹3,500

- Credit card EMI: ₹2,000

His credit score is 760.

Rahul:

- Has stable employment for 3 years

- Maintains regular salary deposits

- Has no missed payments

In this case, Rahul may have a good chance of getting a personal loan because:

- His income is stable

- Existing EMI burden is manageable

- Credit score is healthy

This example shows how lenders evaluate multiple factors together.

Conclusion

Understanding how to check personal loan eligibility before applying can save you from unnecessary rejection and financial stress.

Before applying, always review:

- Your income

- Credit score

- Existing EMIs

- Job stability

- Banking history

Using eligibility calculators and improving weak financial areas can increase your chances of approval.

Most importantly, borrow only what you can comfortably repay. Responsible borrowing helps maintain financial stability and protects your future credit profile.

Frequently Asked Questions (FAQs)

1. What is the minimum credit score needed for a personal loan?

Most lenders prefer a credit score above 700, while 750+ is generally considered better for approval and interest rates.

2. Can I get a personal loan with low income?

Yes, some lenders offer loans for lower-income applicants, but the approved amount may be smaller.

3. Does checking loan eligibility affect my credit score?

Basic eligibility checks and calculator use usually do not affect your score. However, multiple formal applications may impact it.

4. How much salary is required for a personal loan?

The requirement varies by lender. Some banks accept salaries starting from ₹15,000–₹25,000 per month.

5. Can self-employed people apply for personal loans?

Yes, self-employed individuals can apply if they provide proper income proof, bank statements, and business documents.