Taking a loan is common today. People borrow money for buying a home, vehicle, education, smartphone, or even for emergency expenses. However, when you take a loan, you must repay it in small monthly payments. These monthly payments are called EMI.

If you are new to banking or loans, you may wonder: what is EMI and how does it work? Understanding EMI is important because it helps you plan your budget and avoid financial stress later.

In this beginner-friendly guide, you will learn everything about EMI in simple language, including how it is calculated, the factors that affect it, and common mistakes borrowers should avoid.

What Is EMI?

EMI stands for Equated Monthly Installment.

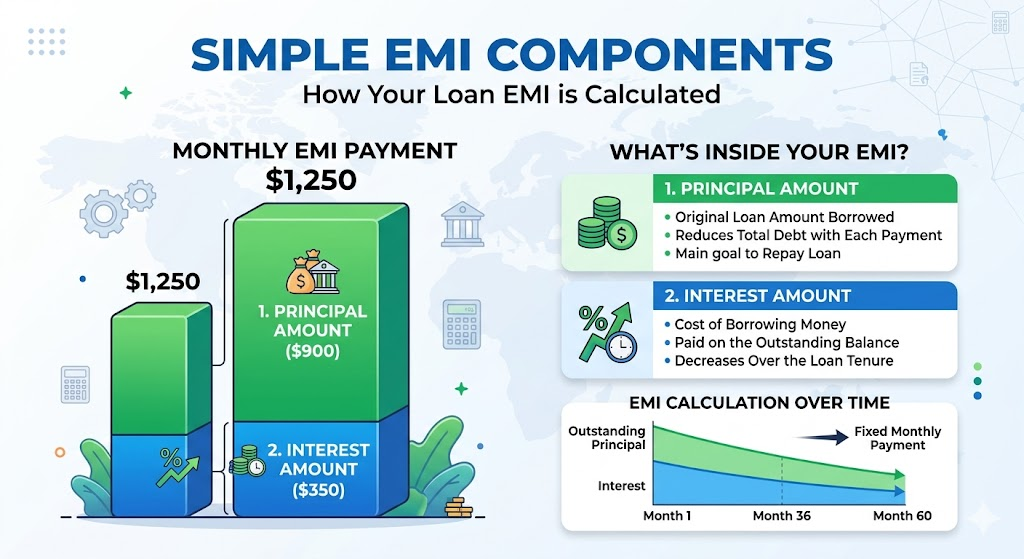

It is a fixed amount of money that a borrower pays every month to repay a loan. The EMI includes:

- A part of the loan amount (principal)

- Interest charged by the bank or lender

The borrower continues paying EMIs every month until the loan is fully repaid.

For example, if you take a personal loan of ₹2 lakh for 3 years, the bank may ask you to pay around ₹6,500 to ₹7,000 every month as EMI depending on the interest rate.

EMIs make loan repayment easier because borrowers do not have to repay the full amount at once.

What Is EMI and How Does It Work?

The answer to what is EMI and how does it work is actually very simple.

When a bank gives you a loan, it charges interest on the borrowed amount. Instead of paying everything together, the bank divides the repayment into equal monthly installments.

Each EMI payment has two parts:

| EMI Component | Meaning |

|---|---|

| Principal | Original loan amount borrowed |

| Interest | Extra amount charged by lender |

At the beginning of the loan period, a larger part of the EMI goes toward interest. As the loan continues, more of the EMI starts reducing the principal amount.

This process continues every month until the loan balance becomes zero.

Most banks automatically deduct EMI from your bank account on a fixed date every month.

Main Components of EMI

To understand EMI properly, you should know its main parts.

1. Principal Amount

This is the original amount borrowed from the lender.

Example:

If you take a loan of ₹5 lakh, then ₹5 lakh is the principal amount.

2. Interest Amount

This is the extra money charged by the bank for lending money to you.

Interest rates may vary depending on:

- Loan type

- Credit score

- Income

- Loan tenure

- Bank policies

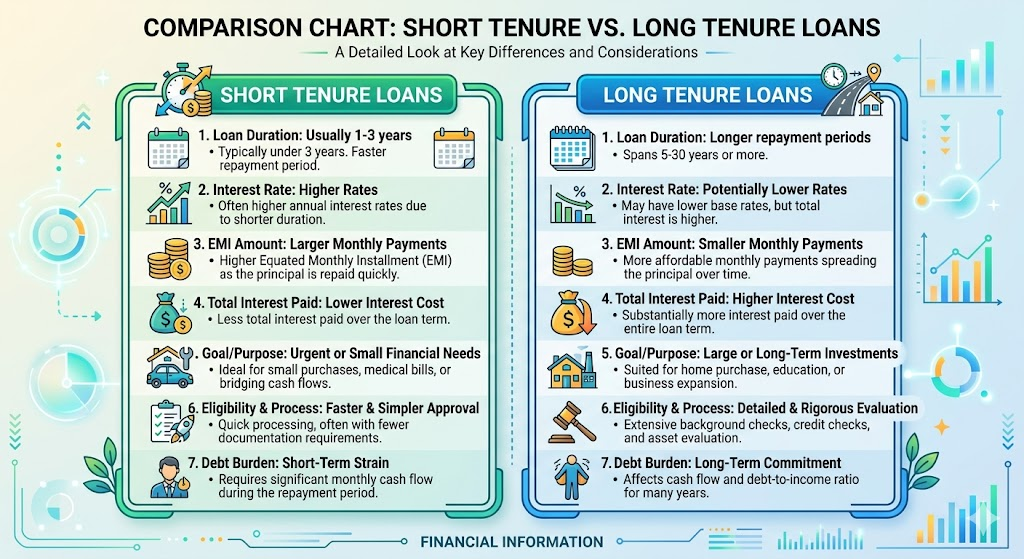

3. Loan Tenure

Loan tenure means the total repayment period.

It can range from:

- Few months

- Few years

- Even 20–30 years for home loans

A longer tenure reduces monthly EMI but increases total interest paid.

How EMI Is Calculated

Banks use a mathematical formula to calculate EMI.

The EMI amount mainly depends on:

- Loan amount

- Interest rate

- Loan tenure

The standard EMI formula is:

EMI=((1+R)N−1)P×R×(1+R)N

Where:

- P = Principal loan amount

- R = Monthly interest rate

- N = Loan tenure in months

You do not need to calculate it manually because banks provide EMI calculators online.

Many borrowers use EMI calculators before applying for loans to understand their monthly repayment burden.

Example of EMI Calculation

Let us understand EMI with a simple example.

| Loan Details | Value |

|---|---|

| Loan Amount | ₹5,00,000 |

| Interest Rate | 10% per year |

| Loan Tenure | 5 years |

In this case, the approximate EMI may be around ₹10,624 per month.

This means:

- You pay ₹10,624 every month

- For 60 months

- Until the loan is fully repaid

At the end of the loan period, the total repayment amount will be higher than ₹5 lakh because interest is included.

Types of Loans That Use EMI

EMIs are used in many types of loans.

Home Loans

Home loans usually have long repayment periods ranging from 10 to 30 years.

If you are planning to buy property, you may also like reading a guide related to home loan eligibility and repayment planning.

Personal Loans

Personal loans often have higher interest rates compared to secured loans.

Borrowers usually choose them for:

- Medical emergencies

- Weddings

- Travel

- Home renovation

You can also explore articles related to personal loan repayment strategies for better financial planning.

Education Loans

Students often repay education loans through EMI after completing studies.

These loans help cover:

- Tuition fees

- Hostel expenses

- Study materials

Car Loans

Vehicle loans are commonly repaid through monthly EMIs over several years.

Consumer Durable Loans

Many electronic products like smartphones, TVs, and laptops are also available on EMI.

Factors That Affect EMI Amount

Several factors influence how much EMI you must pay.

1. Loan Amount

A higher loan amount usually means a higher EMI.

2. Interest Rate

Higher interest rates increase monthly EMI.

Even a small difference in interest rate can significantly affect total repayment.

3. Loan Tenure

Longer tenure lowers EMI but increases total interest cost.

Shorter tenure increases EMI but saves interest in the long run.

4. Credit Score

Your credit score plays a major role in loan approval and interest rates.

People with good credit scores often get lower interest rates and better EMI terms.

You may also find it useful to read about how credit scores affect loan approvals and interest rates.

Fixed EMI vs Floating EMI

There are mainly two types of interest structures.

Fixed EMI

In fixed EMI loans:

- Interest rate remains the same

- EMI amount usually stays constant

This provides predictable monthly payments.

Floating EMI

In floating-rate loans:

- Interest rate changes with market conditions

- EMI amount may increase or decrease

Home loans often use floating interest rates.

Advantages of EMI

EMIs offer several benefits to borrowers.

Easy Repayment

Borrowers can repay loans gradually instead of paying a large amount at once.

Better Financial Planning

Fixed monthly payments help manage monthly budgets more effectively.

Access to Expensive Purchases

People can buy homes, cars, or gadgets even if they cannot pay the full amount immediately.

Flexible Loan Options

Banks offer different loan tenures according to borrower needs.

Disadvantages of EMI

Although EMI is useful, there are also some drawbacks.

Interest Increases Total Cost

The final repayment amount is always higher than the original loan amount.

Long-Term Financial Commitment

Borrowers may remain under repayment pressure for many years.

Missed EMI Affects Credit Score

Late payments can negatively impact credit history.

Extra Charges

Banks may charge penalties for:

- Late EMI payment

- Loan foreclosure

- EMI bounce

Common EMI Mistakes to Avoid

Many borrowers make mistakes while managing EMIs.

Borrowing More Than Needed

Taking a larger loan increases financial burden unnecessarily.

Ignoring Interest Rates

Some borrowers only focus on EMI amount instead of total repayment cost.

Missing EMI Due Dates

Late payments can result in penalties and lower credit scores.

Choosing Very Long Tenure

Long tenure reduces EMI but increases total interest paid significantly.

Not Reading Loan Terms

Always check:

- Processing fees

- Foreclosure charges

- Penalty rules

- Interest type

before signing loan documents.

Tips to Manage EMI Better

Managing EMIs properly can reduce financial stress.

Create a Monthly Budget

Track your income and expenses carefully.

Keep Emergency Savings

Emergency funds help continue EMI payments during unexpected situations.

Avoid Multiple Loans Together

Too many EMIs at the same time can affect financial stability.

Pay Extra When Possible

Part-prepayment can reduce:

- Loan burden

- Interest amount

- Loan tenure

Maintain a Good Credit Score

Timely EMI payments improve your financial profile and help in future loan approvals.

EMI and Credit Score

EMI payments directly affect your credit score.

When you pay EMIs on time:

- Your credit score improves

- Banks trust you more

- Future loan approvals become easier

However, missed or delayed EMIs can lower your score.

A poor credit score may result in:

- Higher interest rates

- Loan rejection

- Lower credit limits

Therefore, responsible EMI management is extremely important for long-term financial health.

How to Choose the Right EMI

Before taking a loan, make sure the EMI fits comfortably within your monthly income.

Financial experts often suggest keeping total EMIs below 40–50% of monthly income.

You should also compare:

- Interest rates

- Processing fees

- Loan tenure

- Prepayment rules

from different banks before choosing a loan.

Using an EMI calculator can also help you understand repayment obligations clearly.

Conclusion

Understanding what is EMI and how does it work is very important before taking any loan. EMI helps borrowers repay loans in smaller monthly installments instead of making one large payment.

However, borrowers should always check loan terms carefully, compare interest rates, and choose EMI amounts that match their financial situation. Responsible EMI management not only reduces financial stress but also improves your credit profile over time.

Whether you are planning for a home loan, education loan, or personal loan, understanding EMI can help you make smarter financial decisions.

FAQs

1. What does EMI mean in banking?

EMI means Equated Monthly Installment. It is the fixed monthly payment made toward loan repayment.

2. Does EMI include interest?

Yes. EMI includes both principal amount and interest charged by the lender.

3. Can EMI amount change during the loan period?

Yes, in floating interest rate loans, EMI may change depending on market interest rates.

4. Is longer loan tenure better?

Longer tenure reduces EMI but increases total interest paid. Shorter tenure saves interest but increases monthly EMI.

5. What happens if I miss an EMI payment?

Missing EMI may lead to penalties, lower credit score, and negative impact on future loan approvals.