Taking an education loan can help students achieve their career goals without putting immediate financial pressure on the family. However, many students and parents feel confused when the repayment stage begins. Terms like EMI, moratorium period, interest rates, and repayment schedules can sound difficult at first.

This guide on the education loan repayment process explained simply will help beginners understand everything in easy language. Whether you are planning to take an education loan or already have one, this article will make the repayment process easier to understand.

A clear understanding of repayment can help you avoid missed payments, reduce stress, and improve your financial future.

What Is an Education Loan Repayment?

Education loan repayment means returning the borrowed loan amount to the bank or lender along with interest. Repayment usually starts after the student completes the course and gets some extra time to find a job.

The repayment is mostly done through monthly installments called EMIs (Equated Monthly Installments).

A typical education loan includes:

| Component | Meaning |

|---|---|

| Principal Amount | The actual borrowed money |

| Interest | Extra amount charged by the lender |

| EMI | Fixed monthly payment |

| Loan Tenure | Total repayment period |

For example, if a student borrows ₹5 lakh for higher studies, the bank may allow repayment over 5 to 10 years after course completion.

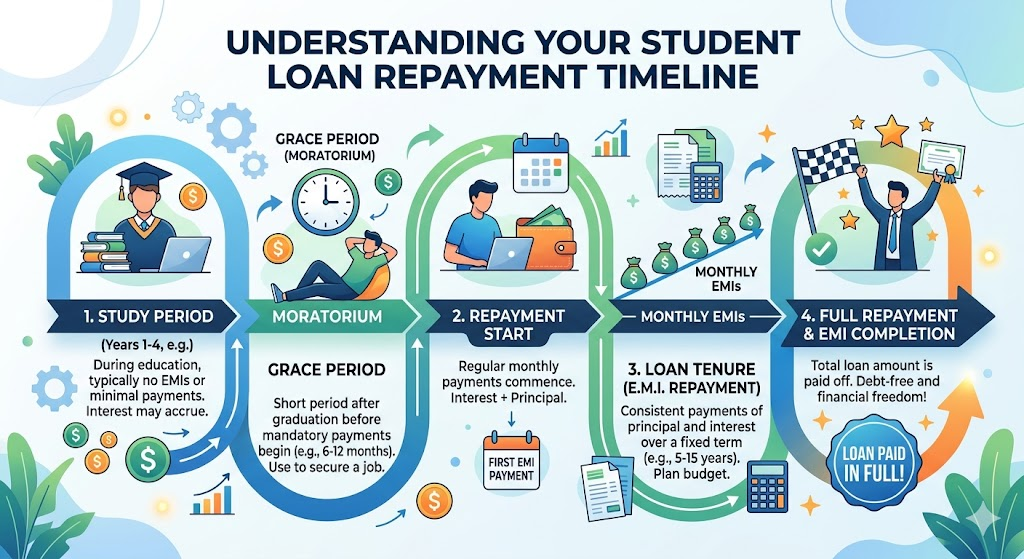

Education Loan Repayment Process Explained Simply

The education loan repayment process is usually simple when broken into steps.

Step 1: Loan Disbursement

The bank releases the approved loan amount directly to the college or university in parts or full.

Step 2: Course Completion

During the study period, students usually do not need to pay full EMIs. Some lenders may ask for simple interest payments during this period.

Step 3: Moratorium Period

After the course ends, banks generally provide a waiting period called a moratorium period. This gives students time to find employment.

This period may include:

- Course duration

- Additional 6 to 12 months after course completion

Step 4: EMI Starts

Once the moratorium period ends, the borrower starts paying EMIs every month.

Step 5: Regular Repayment

The borrower continues paying EMIs until the entire loan and interest amount are cleared.

Banks usually offer online payment options through:

- Net banking

- Auto-debit

- UPI

- Mobile banking apps

Understanding the Moratorium Period

The moratorium period is one of the most important parts of education loans.

It is the time during which students are not required to pay full EMIs.

However, many borrowers misunderstand this period. Interest may still continue adding to the loan during this time.

Types of Payments During Moratorium

| Payment Type | Description |

|---|---|

| No Payment | Interest keeps adding to the loan |

| Simple Interest Payment | Only interest is paid monthly |

| Partial EMI | Small monthly payments |

Paying at least the interest during the moratorium period can reduce the overall loan burden later.

What Is EMI in Education Loans?

EMI stands for Equated Monthly Installment.

It is the fixed amount paid every month to repay the loan.

An EMI includes:

- Part of the principal amount

- Interest charged by the lender

EMI Depends On:

- Loan amount

- Interest rate

- Repayment tenure

For example:

| Loan Amount | Interest Rate | Tenure | Approx EMI |

|---|---|---|---|

| ₹5 lakh | 10% | 7 years | ₹8,300 |

| ₹10 lakh | 11% | 10 years | ₹13,700 |

These numbers are only examples and may vary between lenders.

Different Repayment Methods

Different banks may provide flexible repayment options.

Standard EMI Repayment

This is the most common method. Borrowers pay a fixed EMI every month.

Step-Up Repayment

EMIs start small and increase gradually as the borrower’s salary grows.

Interest-Only Payments Initially

Some lenders allow students to pay only interest during the study period.

Prepayment Option

Borrowers can pay extra money before the loan tenure ends.

Some banks charge no prepayment penalty on education loans.

If you are comparing loans, it is also useful to read about how repayment works in other borrowing categories like personal loans and home loans. Internal guides related to those topics can help readers understand overall loan management better.

Example of Education Loan Repayment

Let us understand with a simple example.

Rahul takes an education loan of ₹8 lakh for engineering studies.

Loan Details

| Item | Value |

|---|---|

| Loan Amount | ₹8 lakh |

| Interest Rate | 10% |

| Course Duration | 4 years |

| Moratorium | 6 months |

| Repayment Tenure | 8 years |

During Studies

Rahul does not pay EMIs during college.

Interest keeps getting added to the loan.

After Graduation

Rahul gets a job after 4 months.

His EMI starts after the moratorium period ends.

He pays around ₹12,000 monthly for 8 years.

If Rahul makes extra payments whenever he receives bonuses, he may finish repayment earlier and save interest costs.

Benefits of Repaying on Time

Timely repayment gives many financial advantages.

Improves Credit Score

Regular EMI payments improve your credit history.

A good credit score helps in future loans such as:

- Home loans

- Car loans

- Personal loans

You can also explore educational content related to credit scores and banking basics to better understand how repayment affects your financial profile.

Reduces Financial Stress

Timely payments help avoid penalty charges and collection calls.

Builds Financial Discipline

Loan repayment teaches budgeting and money management.

Better Loan Eligibility in Future

Banks trust borrowers who repay loans responsibly.

Common Mistakes Users Should Avoid

Many borrowers face repayment problems because of small mistakes.

Ignoring Interest During Study Period

Interest keeps increasing if nothing is paid during the moratorium period.

Missing EMI Due Dates

Late payments can hurt your credit score.

Taking a Larger Loan Than Needed

Borrow only what is necessary for education expenses.

Not Reading Loan Terms Carefully

Always understand:

- Interest type

- Processing fees

- Repayment rules

- Penalty charges

Depending Fully on Future Salary

Job markets can change. Always keep a backup repayment plan.

Tips to Repay Education Loans Faster

Repaying early can save a large amount of interest.

Pay Interest During the Course

Even small payments help reduce future burden.

Make Partial Prepayments

Use bonuses, internships, or freelance income to reduce principal.

Choose Shorter Tenure If Affordable

Shorter tenure usually means lower total interest.

Avoid Missing EMIs

Set automatic payments through your bank account.

Create a Monthly Budget

Track income and expenses carefully after getting a job.

Pros and Cons of Education Loans

Understanding both sides helps borrowers make better decisions.

| Pros | Cons |

|---|---|

| Helps students continue education | Interest increases total repayment |

| Flexible repayment options | Long repayment periods |

| Builds credit history | Missed EMIs affect credit score |

| Tax benefits may apply | Financial pressure after graduation |

Important Things to Check Before Repayment Starts

Before your repayment begins, review these important details carefully.

Loan Balance

Check the total outstanding amount including interest.

EMI Amount

Understand how much you need to pay monthly.

Interest Rate Changes

Some education loans have floating interest rates.

Auto-Debit Setup

Ensure your bank account has enough balance every month.

Repayment Schedule

Keep a copy of your repayment statement safely.

You may also find it useful to learn more about basic banking and finance concepts because understanding interest rates, credit reports, and loan structures can help you manage debt more confidently.

Can You Get Tax Benefits on Education Loan Repayment?

Yes, education loans may offer tax benefits under Indian tax laws.

Under Section 80E of the Income Tax Act, borrowers can claim deductions on interest paid for education loans.

Important Points

- Deduction is available only on interest

- Applicable for higher education loans

- Available for a limited number of years

Tax rules may change over time, so checking with a qualified tax professional is always recommended.

What Happens If You Cannot Repay the Loan?

Sometimes borrowers may face financial difficulties.

If repayment becomes difficult:

Contact the Bank Early

Do not ignore calls or notices.

Ask for Loan Restructuring

Banks may offer:

- Extended tenure

- Temporary relief

- EMI adjustments

Avoid Loan Default

Continuous non-payment can damage your credit profile badly.

Being honest and proactive usually helps borrowers find better solutions.

Conclusion

Understanding the education loan repayment process explained simply can help students and families make smarter financial decisions. Education loans can support career growth, but repayment planning is equally important.

Knowing how EMIs work, understanding the moratorium period, paying on time, and avoiding common mistakes can make the repayment journey much smoother.

Before taking any loan, compare lenders carefully, read the terms properly, and create a realistic repayment plan based on future income and expenses.

Responsible borrowing and timely repayment can improve your financial stability and build a strong credit history for the future.

Read Also: Can Students Get Education Loans Without Collateral?

Frequently Asked Questions (FAQs)

1. When does education loan repayment usually start?

Repayment usually starts after course completion and the moratorium period ends.

2. What happens if I miss an EMI payment?

Missing EMI payments may lead to penalties and can negatively affect your credit score.

3. Can I repay my education loan early?

Yes, many banks allow prepayment or early repayment. Some lenders may not charge prepayment penalties.

4. Is interest charged during the study period?

Yes, in many cases interest continues during the study period and moratorium period.

5. Does education loan repayment improve credit score?

Yes, regular EMI payments can improve your credit history and increase your credit score over time.