Applying for a personal loan may look simple, but many people get rejected without clearly understanding why. If you have ever wondered why personal loan application gets rejected, you are not alone.

Banks and lenders check several things before approving a loan. They want to make sure the borrower can repay the money on time. Even small mistakes in your application can reduce your approval chances.

The good news is that most loan rejections can be avoided. Once you understand the common reasons behind rejection, you can improve your financial profile and apply more confidently in the future.

This beginner-friendly guide explains the most common reasons personal loan applications get rejected, what lenders usually check, and how you can improve your chances of approval.

What Do Lenders Check Before Approving a Personal Loan?

Before approving a personal loan, banks and financial institutions review your financial condition carefully. They mainly want to know whether you can repay the loan comfortably.

Here are some important things lenders usually check:

| Factor | Why It Matters |

|---|---|

| Credit score | Shows your repayment history |

| Monthly income | Helps lenders judge repayment ability |

| Existing loans | Too much debt increases risk |

| Job stability | Stable employment improves trust |

| Loan application details | Incorrect details may cause rejection |

| Bank account history | Poor banking habits may create concern |

If any of these areas look risky, the lender may reject the application.

Why Personal Loan Application Gets Rejected

There are several reasons why banks reject personal loan applications. Let’s understand each one in simple language.

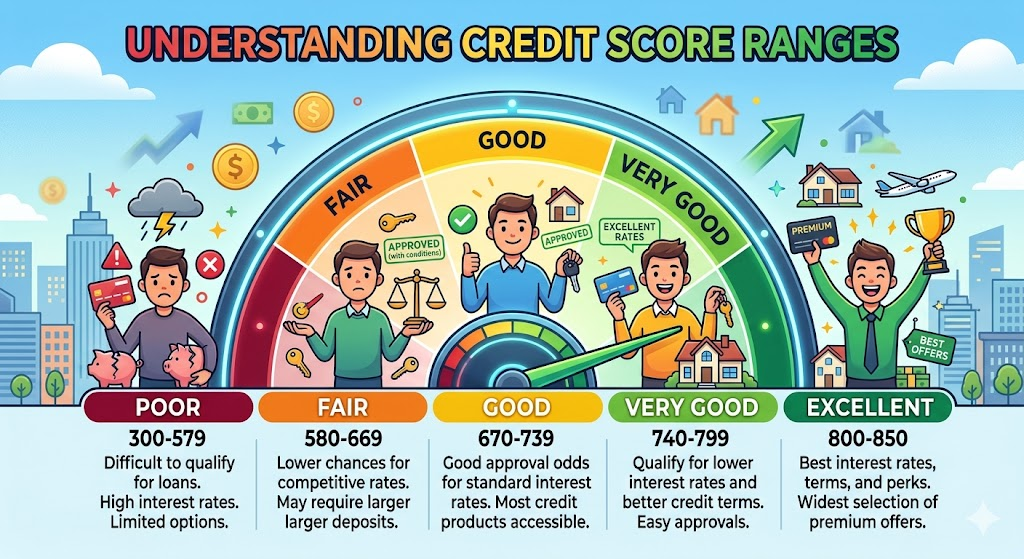

Low Credit Score

A low credit score is one of the biggest reasons for loan rejection.

Your credit score reflects how responsibly you have handled loans and credit cards in the past. If you missed EMIs, delayed payments, or defaulted earlier, your score may fall.

Most lenders prefer borrowers with a good credit score because it lowers their risk.

For example:

- A score above 750 is generally considered good

- A score below 650 may create approval problems

If your score is low, lenders may think you could struggle with repayments.

You can also read more about improving your credit profile in your related article on credit scores and loan eligibility.

Insufficient Income

Even if your credit score is decent, lenders may reject your application if your income is too low.

Banks check whether your salary or business income is enough to handle monthly EMIs along with your current expenses.

For example, if your monthly income is ₹25,000 but your existing EMIs already consume ₹15,000, lenders may see this as risky.

Income requirements vary depending on:

- Loan amount

- City of residence

- Employer type

- Existing financial obligations

Higher income generally improves approval chances.

Too Many Existing Loans

Having multiple active loans can reduce your chances of getting another personal loan.

Lenders calculate something called the debt-to-income ratio. This simply means how much of your monthly income already goes toward debt repayment.

If too much income is already committed to:

- Credit card bills

- Car loans

- Home loans

- Education loans

then lenders may worry that adding another EMI could become difficult for you.

This is one reason many borrowers get rejected even with stable jobs.

Unstable Job or Frequent Job Changes

Job stability matters a lot in loan approval.

If you recently changed jobs multiple times or have very short employment history, lenders may see your income as unstable.

Most banks prefer applicants who:

- Have worked at the same company for at least 6–12 months

- Receive regular monthly salary

- Work with reputed employers

Self-employed individuals may also face rejection if business income is inconsistent.

Errors in the Loan Application

Simple mistakes in the application form can also lead to rejection.

Common mistakes include:

- Wrong PAN or Aadhaar details

- Incorrect income information

- Mismatch in address

- Typing errors

- Missing documents

Sometimes borrowers accidentally enter wrong salary figures or outdated contact details.

Even small errors may delay verification or create trust issues.

Always double-check your application before submitting it.

Poor Repayment History

Your repayment history plays a major role in loan approval.

If you previously:

- Missed EMI payments

- Settled loans instead of fully repaying

- Delayed credit card bills

- Defaulted on loans

then lenders may hesitate to approve a new loan.

Banks usually check your credit report before making a decision.

A poor repayment record tells lenders that lending money to you may involve higher risk.

Applying for Too Many Loans Together

Some people apply for loans with many banks at the same time after facing rejection.

This can actually hurt approval chances further.

Every loan application creates a hard inquiry on your credit report. Too many inquiries within a short period may signal financial stress.

As a result, lenders may become cautious.

Instead of applying everywhere immediately, first understand the reason for rejection and improve your profile.

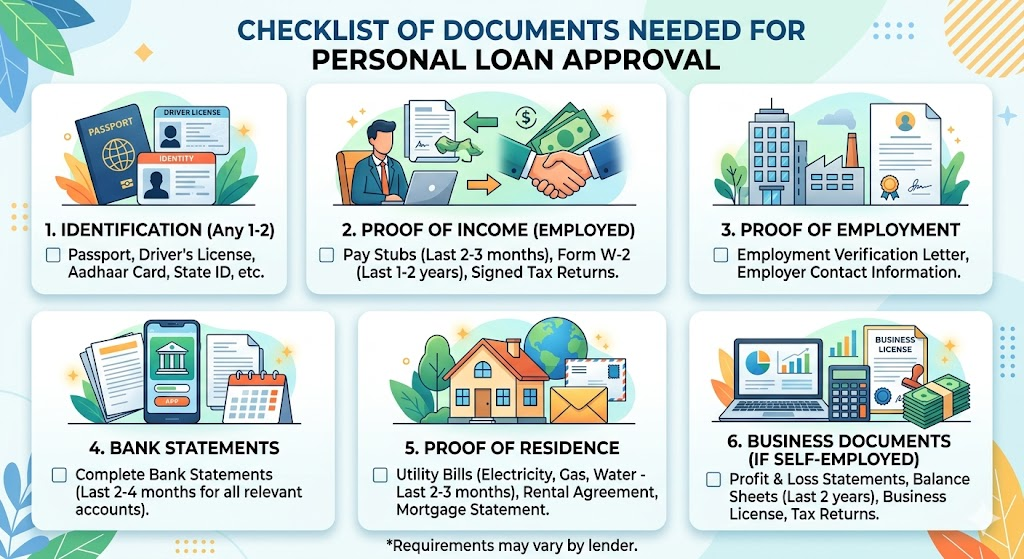

Lack of Proper Documents

Incomplete documentation is another common reason for rejection.

Most lenders ask for:

- Identity proof

- Address proof

- Income proof

- Bank statements

- Employment details

If documents are unclear, outdated, or missing, the lender may reject the application during verification.

Always keep updated financial documents ready before applying.

Loan Amount Is Too High

Sometimes borrowers apply for loan amounts that do not match their income level.

For example, if someone earning ₹30,000 per month applies for a very large personal loan, lenders may feel repayment could become difficult.

Applying for a realistic loan amount improves approval chances.

You can later apply for a higher amount once your income increases or repayment history improves.

Poor Banking Habits

Banks also review your account activity in some cases.

Problems may include:

- Frequent low balance

- Cheque bounces

- Irregular salary credits

- Excessive overdrafts

These patterns may create concerns about financial management.

Maintaining a healthy bank account can improve lender confidence.

Common Mistakes Borrowers Should Avoid

Many rejections happen because borrowers make avoidable mistakes.

Here are some common ones:

Ignoring Credit Score

Many first-time borrowers apply without checking their credit score.

It is always better to review your score first before applying.

Applying in Panic

Applying to many lenders quickly after rejection usually creates more problems.

Instead, improve your financial profile first.

Providing Incorrect Information

Never exaggerate income or provide false details.

Lenders verify most information carefully.

Incorrect details can lead to immediate rejection.

Taking Too Much Debt

Borrow only what you truly need.

Large debts can become difficult to manage later.

How to Improve Your Loan Approval Chances

If your application was rejected earlier, do not lose hope. There are several ways to improve your chances in the future.

Improve Your Credit Score

Pay all EMIs and credit card bills on time.

Avoid missing payments.

A better credit score increases lender confidence.

Reduce Existing Debt

Try to close smaller loans or reduce credit card balances before applying again.

Lower debt improves your debt-to-income ratio.

Maintain Stable Employment

Job stability helps lenders trust your repayment ability.

Avoid frequent job switching before applying for a major loan.

Apply for a Smaller Amount

A smaller loan amount may have better approval chances.

You can gradually build a strong repayment history.

Keep Documents Ready

Ensure all documents are updated and accurate before applying.

This helps avoid verification issues.

Compare Lenders Carefully

Different lenders have different eligibility rules.

Research properly before applying.

You may also find useful guidance in your related articles on personal loan eligibility and banking basics.

Should You Apply Again After Rejection?

Yes, but not immediately without understanding the reason.

First:

- Check why your application was rejected

- Improve weak areas

- Correct mistakes if any

- Wait for your financial profile to improve

Applying again too quickly without improvement may reduce approval chances further.

In some cases, waiting a few months and improving your credit behavior can make a big difference.

Pros and Cons of Personal Loans

| Pros | Cons |

|---|---|

| Useful during emergencies | Interest rates may be high |

| Usually requires no collateral | Poor repayment affects credit score |

| Flexible usage | Extra debt burden |

| Fixed repayment schedule | Rejection possible for low credit profile |

Tips Before Applying for a Personal Loan

Here are some practical beginner-friendly tips:

- Check your credit score first

- Borrow only what you need

- Compare loan offers carefully

- Read terms and charges properly

- Avoid multiple applications together

- Keep emergency savings separately

- Maintain timely repayments

Small financial habits can improve your approval chances over time.

Conclusion

Understanding why personal loan application gets rejected can help you avoid common mistakes and improve your financial profile before applying again.

Most rejections happen due to low credit scores, high existing debt, unstable income, documentation errors, or poor repayment history. The good part is that many of these issues can be corrected with better financial planning and responsible borrowing habits.

Before applying for a personal loan, take time to review your finances carefully. A stronger financial profile not only improves approval chances but also helps you manage repayments more comfortably in the future.

FAQs

1. What is the most common reason for personal loan rejection?

The most common reason is usually a low credit score or poor repayment history.

2. Can I get a personal loan with a low salary?

Yes, but approval depends on your debt level, credit score, and lender requirements.

3. Does loan rejection affect credit score?

A single rejection usually does not reduce your score directly, but multiple loan applications in a short time may affect it.

4. How long should I wait before applying again?

It is better to wait until you improve the reason behind rejection, such as reducing debt or improving your credit score.

5. Can incorrect documents cause loan rejection?

Yes. Wrong or incomplete documents can delay verification and lead to rejection.

Also Read: Documents Required for Personal Loan for Salaried People