Buying a home is one of the biggest financial decisions most people make. While choosing the right property is important, selecting the right type of home loan interest rate is equally important.

Many first-time borrowers often get confused between fixed and floating interest rates. Banks usually offer both options, but understanding how they work can help you save money over the long term.

In this guide, we will explain fixed vs floating home loan interest rate explained in very simple language. You will learn how both interest rate types work, their advantages and disadvantages, and which one may suit your financial situation better.

Whether you are planning to buy your first house or refinance an existing loan, this article will help you make a smarter decision.

What Is a Home Loan Interest Rate?

A home loan interest rate is the amount a bank or lender charges you for borrowing money to purchase a property.

For example, if you take a home loan of $200,000 with a 7% interest rate, you will repay the original loan amount plus interest over time.

Your interest rate directly affects:

- Your monthly EMI or mortgage payment

- Total repayment amount

- Loan affordability

- Long-term financial planning

That is why understanding interest rates is extremely important before signing a loan agreement.

What Is a Fixed Home Loan Interest Rate?

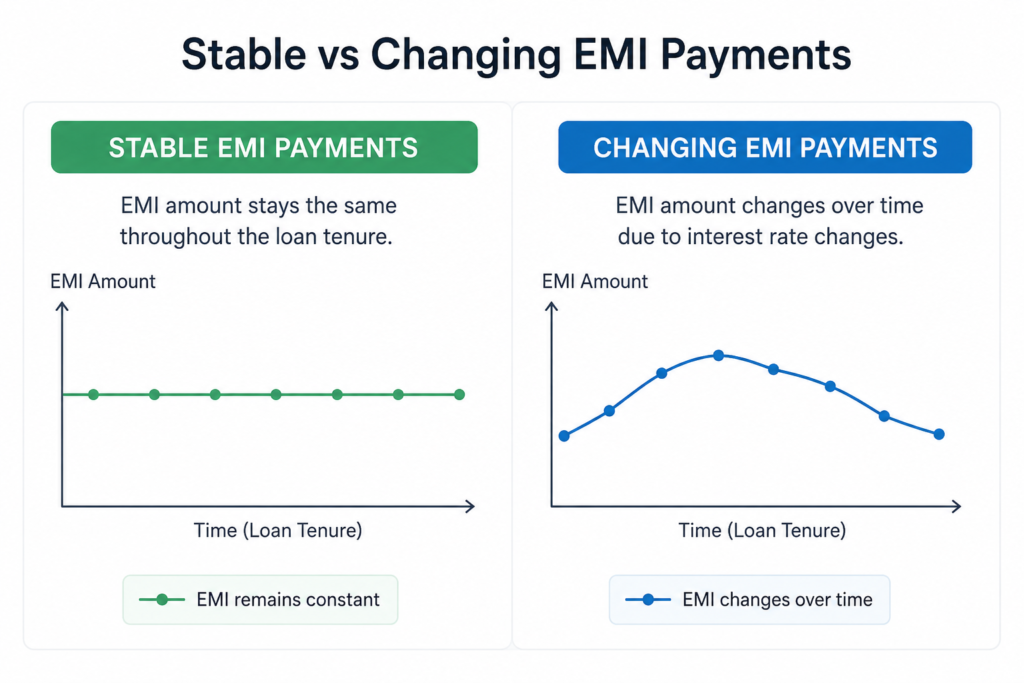

A fixed home loan interest rate remains the same throughout a specific period of the loan.

For example:

- You take a loan at 7.5% interest

- The bank locks this rate for 5 years

- Even if market rates increase or decrease, your interest rate stays unchanged during that period

This option provides payment stability because your monthly EMI remains predictable.

Example

Suppose you borrow $250,000 at a fixed interest rate of 7%.

Your EMI will stay almost the same during the fixed-rate period, regardless of changes in market conditions.

What Is a Floating Home Loan Interest Rate?

A floating interest rate changes according to market conditions and central bank policies.

If market interest rates go up, your loan interest rate may increase. Similarly, if rates fall, your EMI may reduce.

Floating rates are usually linked to benchmark lending rates set by banks or financial institutions.

Example

You take a home loan at a floating rate of 6.8%.

- If market rates increase, your interest rate may rise to 7.3%

- If rates decrease, it may fall to 6.3%

This means your EMI may change over time.

Fixed vs Floating Home Loan Interest Rate Explained

Understanding the difference between fixed and floating rates can help you choose the right loan structure for your financial goals.

| Feature | Fixed Interest Rate | Floating Interest Rate |

|---|---|---|

| Interest Rate | Remains stable | Changes with market |

| EMI Amount | Mostly fixed | May increase or decrease |

| Risk Level | Lower uncertainty | Higher uncertainty |

| Initial Interest Rate | Usually higher | Usually lower |

| Best For | Stable income earners | Flexible borrowers |

| Benefit When Rates Fall | No | Yes |

| Budget Planning | Easier | Slightly difficult |

Both options have benefits and risks. The right choice depends on your financial stability, risk tolerance, and future interest rate expectations.

Advantages and Disadvantages of Fixed Rates

Advantages of Fixed Home Loan Rates

1. Predictable Monthly Payments

Your EMI stays stable during the fixed period. This helps with budgeting and long-term planning.

2. Protection From Market Increases

If market interest rates rise sharply, your loan cost does not increase.

3. Better for First-Time Buyers

Beginners often prefer fixed rates because they are easier to understand and manage.

Disadvantages of Fixed Home Loan Rates

1. Higher Initial Interest Rate

Banks usually charge slightly higher fixed rates compared to floating rates.

2. Limited Benefit if Rates Fall

Even if market rates decrease, your interest rate remains unchanged.

3. Possible Prepayment Charges

Some lenders may charge penalties for early repayment or refinancing.

Advantages and Disadvantages of Floating Rates

Advantages of Floating Home Loan Rates

1. Lower Initial Rates

Floating rates are often cheaper at the beginning of the loan.

2. Benefit From Falling Interest Rates

If market rates decline, your EMI or loan tenure may reduce.

3. Usually Fewer Prepayment Charges

Many lenders offer flexible repayment options on floating-rate loans.

Disadvantages of Floating Home Loan Rates

1. EMI Can Increase

Rising market rates can increase your monthly payments.

2. Difficult Financial Planning

Because the interest rate changes, future payments become less predictable.

3. Long-Term Uncertainty

Borrowers with tight budgets may feel stressed during periods of rising interest rates.

Which Option Is Better for You?

There is no single answer for everyone. The best option depends on your income stability, financial goals, and risk comfort.

Choose Fixed Interest Rate If:

- You prefer stable monthly payments

- You have a fixed salary and strict budget

- You are a first-time home buyer

- You expect market rates to rise

Choose Floating Interest Rate If:

- You can handle EMI fluctuations

- You expect rates to fall in the future

- You want lower starting interest rates

- You plan to repay the loan early

Some banks also offer hybrid loans, where part of the loan remains fixed and the rest stays floating.

Practical Example for Better Understanding

Let’s compare two borrowers.

Borrower A: Fixed Rate

- Loan Amount: $300,000

- Interest Rate: 7.5%

- EMI stays stable

Borrower A enjoys predictable payments even if market rates rise.

Borrower B: Floating Rate

- Loan Amount: $300,000

- Starting Interest Rate: 6.9%

Initially, Borrower B pays lower EMI. However, if rates rise later, monthly payments may increase.

This example shows that both options carry different advantages depending on economic conditions.

Common Mistakes to Avoid

Many borrowers focus only on getting loan approval and ignore important details. Here are common mistakes you should avoid.

1. Choosing Only Based on Lower EMI

A lower EMI today may become expensive later if floating rates increase significantly.

2. Ignoring Loan Terms

Always read:

- Rate reset clauses

- Processing fees

- Prepayment charges

- Conversion fees

3. Not Comparing Multiple Lenders

Different banks offer different rates and loan structures.

Comparing offers can help you save thousands over the loan period.

4. Ignoring Credit Score

A better credit score may help you qualify for lower interest rates.

You can also read our guide on improving your credit score before applying for a home loan.

5. Borrowing Beyond Your Capacity

Choose an EMI amount that comfortably fits your monthly budget.

Helpful Tips Before Choosing a Home Loan Interest Rate

Understand the Current Interest Rate Trend

If interest rates are expected to rise, fixed rates may offer better protection.

If rates are expected to fall, floating rates may become cheaper.

Calculate Total Loan Cost

Do not focus only on monthly EMI.

Check:

- Total repayment amount

- Loan tenure

- Hidden charges

- Insurance costs

Maintain a Strong Credit Profile

Good financial habits improve loan eligibility and may reduce interest costs.

You may also explore articles related to personal loans and banking & finance basics to improve your overall financial understanding.

Use a Home Loan EMI Calculator

An EMI calculator helps estimate monthly payments under different interest rate scenarios.

Review Your Financial Stability

Stable income earners often prefer fixed rates, while flexible earners may manage floating rates more comfortably.

Conclusion

Understanding fixed vs floating home loan interest rate explained is important before taking any long-term home loan.

Fixed interest rates provide stability and predictable monthly payments, making them suitable for borrowers who prefer financial certainty.

On the other hand, floating interest rates may offer lower starting costs and potential savings when market rates decline.

Before choosing any loan type, compare lenders carefully, understand the terms clearly, and evaluate your financial comfort level.

A well-informed decision today can help you manage your home loan more confidently for many years.

(FAQs)

1. Which is safer: fixed or floating home loan interest rate?

Fixed rates are generally considered safer because monthly payments remain stable during the fixed period.

2. Are floating interest rates always cheaper?

Not always. Floating rates may start lower, but they can increase later depending on market conditions.

3. Can I switch from fixed to floating interest rate later?

Yes, many banks allow conversion, but there may be processing or conversion charges.

4. Which option is better for first-time home buyers?

Many first-time buyers prefer fixed rates because budgeting becomes easier.

5. Do fixed interest rates stay fixed forever?

Not always. Some lenders offer fixed rates only for a certain number of years before converting to floating rates.

Read Also: How Much Down Payment Is Needed for a Home Loan?

Vivek Malik is a finance content writer and researcher who focuses on creating simple and beginner-friendly articles about loans, credit scores, banking, and personal finance. He aims to help readers understand financial topics in clear and easy language through practical and informative guides.