Many people use credit cards for shopping, bill payments, travel bookings, and online purchases. However, few understand how credit card habits can influence their credit health.

If you are wondering how credit card usage affects CIBIL score, the answer is simple: the way you use and manage your credit card can either improve your score or lower it over time.

A good CIBIL score can help you get easier approval for loans, better interest rates, and higher chances of qualifying for financial products. On the other hand, poor credit card management can damage your credit profile and make borrowing more difficult.

In this guide, you will learn how credit cards impact your CIBIL score, the mistakes to avoid, and practical tips to maintain a healthy credit profile.

What Is a CIBIL Score?

A CIBIL score is a three-digit number that reflects your creditworthiness. It is generally calculated based on your credit history and borrowing behavior.

Most lenders look at your score before approving:

- Personal loans

- Home loans

- Education loans

- Credit cards

- Business loans

Generally, a score above 750 is considered good by many lenders.

The score is influenced by factors such as:

- Payment history

- Credit utilization

- Credit mix

- Length of credit history

- New credit applications

Why Credit Card Usage Matters

Your credit card activity is regularly reported to credit bureaus. Every month, information such as outstanding balances, payments, and credit limits may be shared.

As a result, your credit card becomes one of the most important factors affecting your credit score.

Even if you do not have a loan, responsible credit card usage can help build a positive credit history.

How Credit Card Usage Affects CIBIL Score

Understanding how credit card usage affects CIBIL score can help you make better financial decisions.

Several factors come into play.

Timely Payments

Payment history is one of the most important factors affecting your credit score.

When you pay your credit card bill on time:

- It shows financial discipline.

- It builds trust with lenders.

- It improves your credit profile over time.

Example

Suppose your monthly credit card bill is ₹8,000.

If you consistently pay the full amount before the due date, your payment record remains positive, which may help your score.

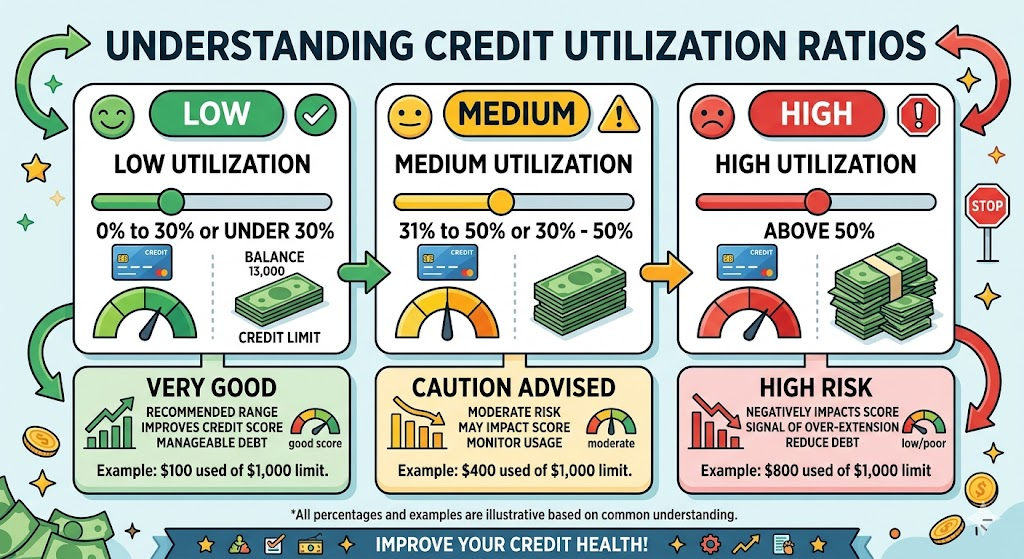

Credit Utilization Ratio

Credit utilization refers to how much of your available credit limit you use.

It is calculated using this formula:

| Credit Limit | Amount Used | Utilization Ratio |

|---|---|---|

| ₹1,00,000 | ₹20,000 | 20% |

| ₹1,00,000 | ₹70,000 | 70% |

A lower utilization ratio generally indicates responsible credit management.

Many financial experts recommend keeping utilization below 30%.

Length of Credit History

Older credit card accounts contribute to a longer credit history.

A longer history allows lenders to evaluate your financial behavior over time.

Closing your oldest credit card may sometimes reduce the average age of your credit accounts.

Credit Inquiries

Applying for multiple credit cards within a short period can result in several hard inquiries.

Too many inquiries may signal increased credit dependence and can negatively affect your score.

Therefore, apply for new credit only when genuinely needed.

Outstanding Balances

Carrying large unpaid balances for extended periods may indicate financial stress.

Even if you make minimum payments, consistently high outstanding balances can affect your credit profile.

Positive Effects of Responsible Credit Card Usage

When used wisely, credit cards can strengthen your credit history.

Builds Credit History

Regular and responsible use creates a track record that lenders can evaluate.

Improves Loan Eligibility

A healthy credit profile may improve your chances of qualifying for:

- Personal loans

- Home loans

- Vehicle loans

- Education loans

For example, readers interested in borrowing for studies may also find our guide on Education Loans useful.

Helps Maintain Good Credit Utilization

Using only a small portion of your available credit limit demonstrates responsible borrowing behavior.

Creates Financial Flexibility

Credit cards can help manage short-term expenses while maintaining a positive repayment record.

Negative Effects of Poor Credit Card Usage

Poor credit card habits can have long-term consequences.

Late Payments

Missing payment due dates can negatively affect your score.

Repeated delays can have an even greater impact.

Maxing Out Credit Cards

Using nearly all available credit limits may indicate higher credit risk.

Example

If your limit is ₹50,000 and you consistently use ₹48,000, lenders may view this negatively.

Frequent Credit Applications

Applying for several credit cards in a short period may lower your score temporarily.

Defaulting on Payments

Failure to repay outstanding balances can severely damage your credit profile.

Defaults may remain visible in credit reports for years.

Credit Utilization Ratio Explained

One of the most misunderstood aspects of credit scoring is credit utilization.

What Is a Good Utilization Ratio?

| Utilization Ratio | Impact on Credit Score |

| Below 30% | Generally Positive |

| 30%–50% | Moderate Impact |

| Above 50% | Potentially Negative |

| Above 75% | Higher Risk Signal |

Practical Example

Assume your credit card limit is ₹2,00,000.

- Spending ₹20,000 = 10% utilization

- Spending ₹50,000 = 25% utilization

- Spending ₹1,60,000 = 80% utilization

The first two scenarios are generally viewed more positively than the third.

Common Credit Card Mistakes to Avoid

Many people unintentionally harm their credit score through simple mistakes.

Avoid these common errors:

- Missing payment due dates

- Paying only the minimum amount regularly

- Using the entire credit limit

- Applying for multiple cards unnecessarily

- Ignoring credit card statements

- Closing old credit cards without proper evaluation

- Carrying high balances month after month

Tips to Improve Your CIBIL Score Using Credit Cards

Improving your score often starts with better credit card habits.

Pay Bills on Time

Set reminders or automatic payments to avoid missed due dates.

Keep Utilization Low

Try to keep spending below 30% of your available credit limit.

Monitor Your Credit Report

Regularly review your credit report for errors or incorrect information.

Avoid Unnecessary Applications

Apply for new credit only when necessary.

Maintain Older Accounts

Keeping older accounts active can contribute to a longer credit history.

Pay More Than the Minimum Due

Whenever possible, pay the full outstanding balance.

Use Credit Responsibly

Spend only what you can comfortably repay.

Readers looking to understand broader credit management may also benefit from our Credit Score guides and Banking & Finance resources.

If you are planning to purchase a property in the future, learning about credit scores can also help when applying for Home Loans.

Pros and Cons of Credit Card Usage

| Pros | Cons |

| Helps build credit history | Late payments can reduce score |

| Improves financial flexibility | High utilization may hurt credit profile |

| Useful for emergencies | Overspending can lead to debt |

| Can improve loan eligibility | Multiple applications may affect score |

| Provides convenience for payments | Interest charges may increase costs |

Conclusion

Understanding how credit card usage affects CIBIL score is essential for maintaining good financial health.

Credit cards are not harmful by themselves. In fact, when used responsibly, they can help build a strong credit history and improve your chances of qualifying for future loans. The key is to pay bills on time, maintain a low credit utilization ratio, avoid unnecessary applications, and monitor your credit profile regularly.

Small financial habits practiced consistently can make a significant difference over time. By managing your credit card wisely, you can work toward a healthier CIBIL score and stronger financial credibility.

Read Also: Minimum CIBIL Score Required for Personal Loans

Frequently Asked Questions (FAQs)

1. Does using a credit card improve a CIBIL score?

Yes. Responsible usage, timely payments, and low credit utilization can help improve your credit profile over time.

2. What is the ideal credit utilization ratio?

Many experts recommend keeping credit utilization below 30% of your total available credit limit.

3. Can missing one credit card payment affect my CIBIL score?

Yes. Even a single missed payment can negatively impact your credit score, especially if it remains unpaid for an extended period.

4. Is it bad to use a credit card every day?

No. Daily usage is not a problem if you manage spending responsibly and pay bills on time.

5. Should I close an old credit card that I no longer use?

Not always. Older accounts contribute to your credit history length, which can be beneficial for your credit profile.

Leave a Reply