Being self-employed gives you freedom and flexibility. However, when it comes to borrowing money, many business owners, freelancers, and professionals often wonder: can self employed person get personal loan easily?

The good news is that self-employed individuals can absolutely apply for personal loans. In fact, many banks and financial institutions offer loans specifically designed for self-employed applicants. However, getting approved may sometimes be slightly different compared to salaried employees because lenders carefully evaluate income stability and repayment ability.

In this guide, you will learn how personal loans work for self-employed people, the eligibility criteria, required documents, common challenges, and practical tips to improve your chances of approval.

What Is a Personal Loan?

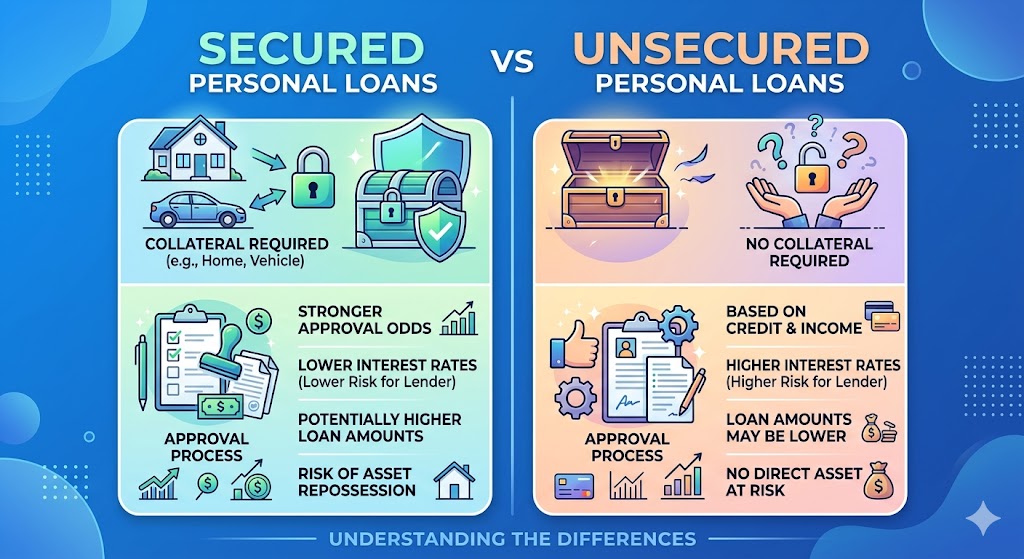

A personal loan is an unsecured loan that allows you to borrow money without providing collateral such as property or gold. You can use the loan amount for various purposes, including:

- Business expansion

- Medical emergencies

- Travel expenses

- Home renovation

- Debt consolidation

- Education expenses

Since personal loans do not require security, lenders focus heavily on your income, credit score, and repayment history.

If you’re new to borrowing, you may also want to read our guide on how personal loans work and their repayment terms.

Can Self Employed Person Get Personal Loan Easily?

The simple answer is yes, but approval depends on several factors.

If you have a stable income, good financial records, and a healthy credit profile, getting a personal loan can become much easier. Banks understand that self-employed individuals earn differently from salaried employees. Therefore, they often assess business income instead of monthly salary slips.

Some self-employed categories that commonly apply for personal loans include:

- Freelancers

- Shop owners

- Consultants

- Doctors

- Chartered accountants

- Small business owners

- Online sellers

- Contractors

Although the process may involve additional document verification, many self-employed people successfully obtain personal loans every year.

Why Lenders Evaluate Self-Employed Applicants Differently

Unlike salaried employees who receive fixed monthly salaries, self-employed income may vary from month to month.

Lenders want to ensure that borrowers can repay loans on time. Therefore, they examine:

- Business stability

- Annual income

- Profit trends

- Existing debts

- Tax records

- Credit history

For example, a freelance graphic designer earning consistently for three years may have better approval chances than someone who recently started a business.

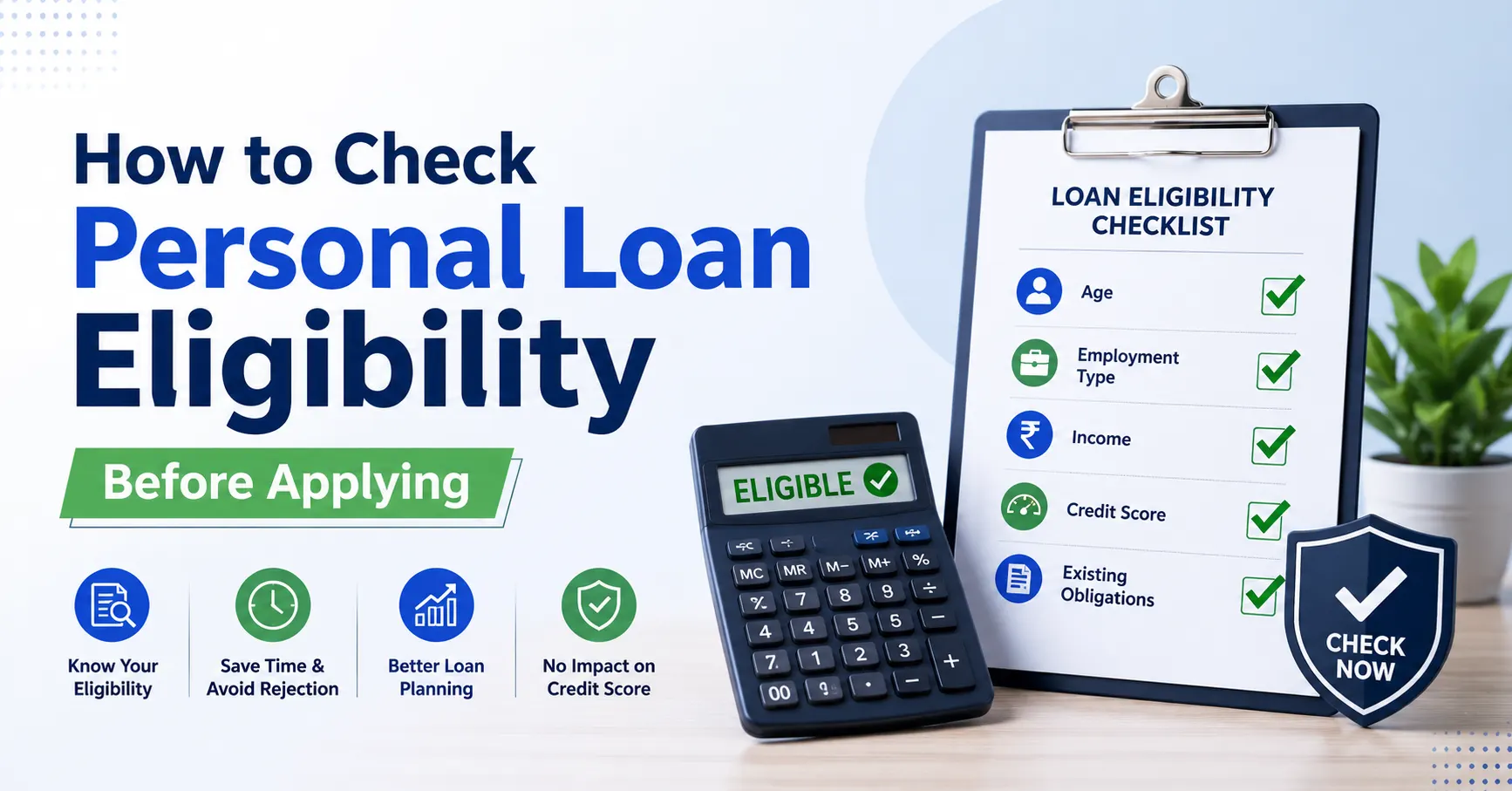

Eligibility Criteria for Self-Employed Borrowers

Each lender has its own requirements, but common eligibility criteria include:

| Eligibility Factor | Typical Requirement |

|---|---|

| Age | 21–65 years |

| Business Experience | 2–3 years minimum |

| Minimum Income | Varies by lender |

| Credit Score | Preferably 700+ |

| Business Stability | Consistent income |

| Nationality | Resident citizen |

Meeting these requirements does not guarantee approval, but it significantly improves your chances.

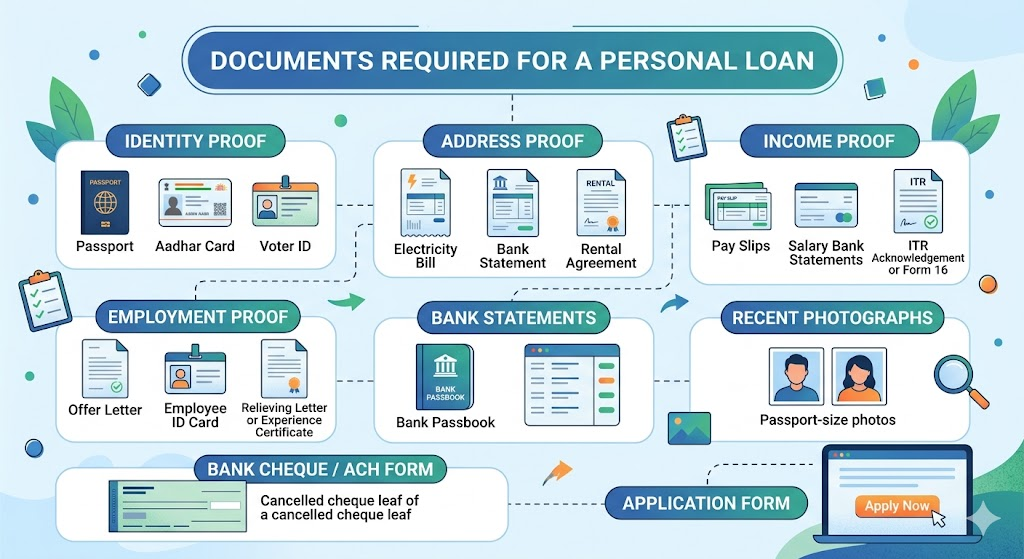

Documents Required for Self-Employed Personal Loans

Self-employed applicants often need more documentation than salaried individuals.

Identity Proof

Examples include:

- Passport

- Driver’s license

- National ID card

Address Proof

Accepted documents may include:

- Utility bills

- Rental agreement

- Government-issued ID

Income Documents

Lenders may ask for:

- Bank statements of the last 6–12 months

- Income tax returns (ITR)

- Profit and loss statements

- Balance sheets

- Business registration proof

Keeping these documents updated can speed up the application process.

Factors That Affect Personal Loan Approval

Several factors influence whether your application gets approved.

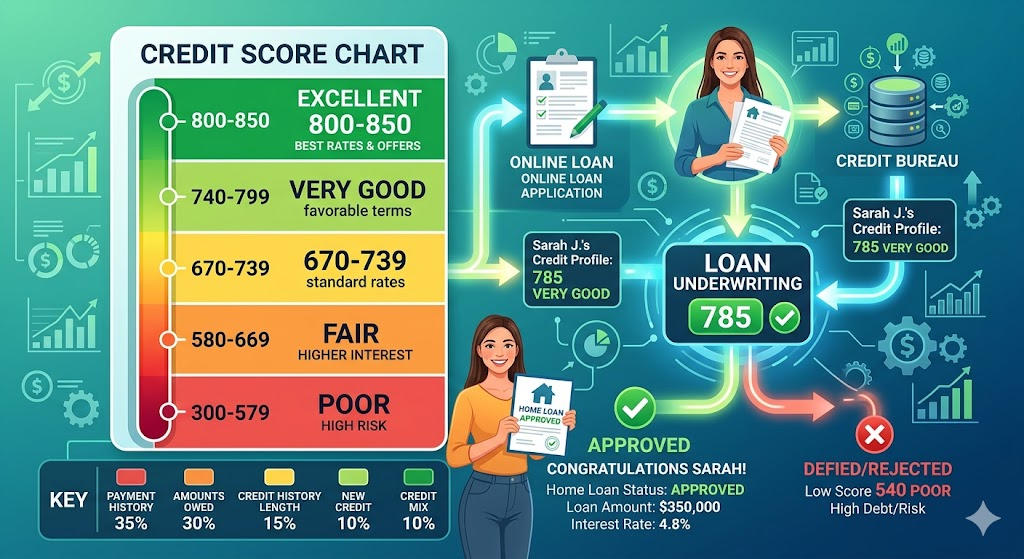

1. Credit Score

A good credit score shows responsible borrowing behavior.

Generally:

- Above 750: Excellent

- 700–750: Good

- Below 650: May face difficulty

You may also explore our detailed guide on how credit scores affect loan approvals and interest rates.

2. Income Stability

Lenders prefer borrowers with stable and predictable earnings.

Consistent bank deposits and regular tax filings strengthen your profile.

3. Debt-to-Income Ratio

If you already have multiple loans or credit card balances, lenders may consider you a higher-risk borrower.

4. Business Vintage

Businesses operating for several years often receive better consideration.

5. Banking History

Maintaining a healthy bank account with regular transactions creates trust with lenders.

Practical Example

Suppose Rahul owns a small digital marketing agency.

- Business age: 4 years

- Credit score: 760

- Annual income: Stable

- Tax returns filed regularly

Rahul is likely to have better chances of receiving a personal loan compared to someone whose business is only six months old and lacks financial records.

This example highlights why financial discipline matters.

Tips to Increase Your Loan Approval Chances

Getting approved becomes easier when you prepare in advance.

Maintain a Good Credit Score

Pay EMIs and credit card bills on time.

File Tax Returns Regularly

Income tax returns help lenders verify your earnings.

Keep Business Accounts Organized

Clear financial records increase lender confidence.

Reduce Existing Debt

Try paying off smaller loans before applying.

Apply for the Right Loan Amount

Borrow only what you genuinely need and can repay comfortably.

Compare Multiple Lenders

Interest rates and eligibility conditions vary among lenders.

If you’re planning a major purchase, you may also compare personal loans with home loan financing options to understand which suits your needs better.

Pros and Cons of Personal Loans for Self-Employed Individuals

| Pros | Cons |

| No collateral required | Income verification can be stricter |

| Flexible usage | Interest rates may vary |

| Quick processing in many cases | More documentation needed |

| Fixed repayment schedule | Lower approval for unstable income |

| Can improve credit history | Existing debts affect eligibility |

Understanding both advantages and disadvantages helps you make informed financial decisions.

Common Mistakes to Avoid

Many applicants unintentionally reduce their chances of approval.

Avoid these common mistakes:

Applying to Too Many Lenders

Multiple loan applications within a short period may impact your credit profile.

Providing Incorrect Information

Always ensure your application details match official documents.

Ignoring Credit Score

Check your credit report before applying.

Borrowing Beyond Capacity

A higher loan amount means higher EMIs.

Not Maintaining Financial Records

Incomplete records may delay or reduce approval chances.

If you are funding education expenses, consider reviewing education loan options and eligibility criteria before choosing a personal loan.

Additional Tips for Self-Employed Borrowers

Here are some extra strategies that can help:

- Maintain separate personal and business bank accounts.

- Build a long-term relationship with your bank.

- Keep emergency savings.

- Monitor your credit report regularly.

- Improve business cash flow consistency.

Small improvements in financial management can make a big difference during loan applications.

Read Also: How to Check Personal Loan Eligibility Before Applying

Frequently Asked Questions (FAQs)

1. Can freelancers apply for personal loans?

Yes. Freelancers can apply if they meet income, business experience, and credit score requirements.

2. What credit score is good for a self-employed personal loan?

A credit score above 700 is generally preferred, while 750 or above may improve approval chances.

3. Do self-employed people need collateral for personal loans?

Most personal loans are unsecured, meaning collateral is usually not required.

4. How many years of business are needed for a loan?

Many lenders prefer at least 2–3 years of business operation, although requirements differ.

5. Can irregular income affect loan approval?

Yes. Lenders prefer stable income because it indicates repayment ability.

Conclusion

So, can self employed person get personal loan easily? The answer is yes—provided they demonstrate stable income, maintain a good credit score, file taxes regularly, and keep financial records organized.

While self-employed applicants may face slightly stricter checks than salaried individuals, many lenders actively offer personal loans to entrepreneurs, freelancers, and small business owners. By understanding lender requirements and improving your financial profile, you can significantly increase your chances of approval.

Borrow responsibly, compare lenders carefully, and choose a loan that fits your financial situation.

Leave a Reply