When applying for a loan, one of the first things you may come across is the choice between a secured and an unsecured personal loan. For many beginners, these terms can sound confusing. However, understanding them is important because the type of loan you choose can affect your interest rate, approval chances, borrowing limit, and financial risk.

In simple words, the difference between secured and unsecured personal loan options comes down to whether you provide an asset as security for the loan.

Both types of loans have advantages and disadvantages. The right choice depends on your financial situation, credit history, and borrowing needs.

In this guide, we will explain everything in simple language so you can make a more informed borrowing decision.

What Is a Personal Loan?

A personal loan is money borrowed from a bank, credit union, or lender that is repaid in fixed monthly installments over a specific period.

People commonly use personal loans for:

- Medical expenses

- Home improvements

- Debt consolidation

- Emergency expenses

- Education-related costs

- Major purchases

Personal loans generally fall into two categories:

- Secured personal loans

- Unsecured personal loans

Let’s understand each one in detail.

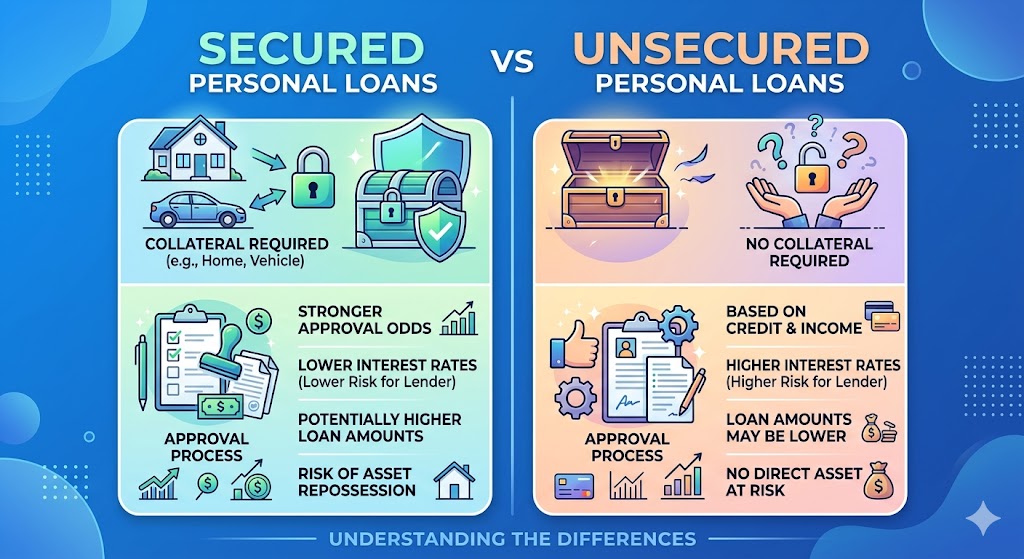

What Is a Secured Personal Loan?

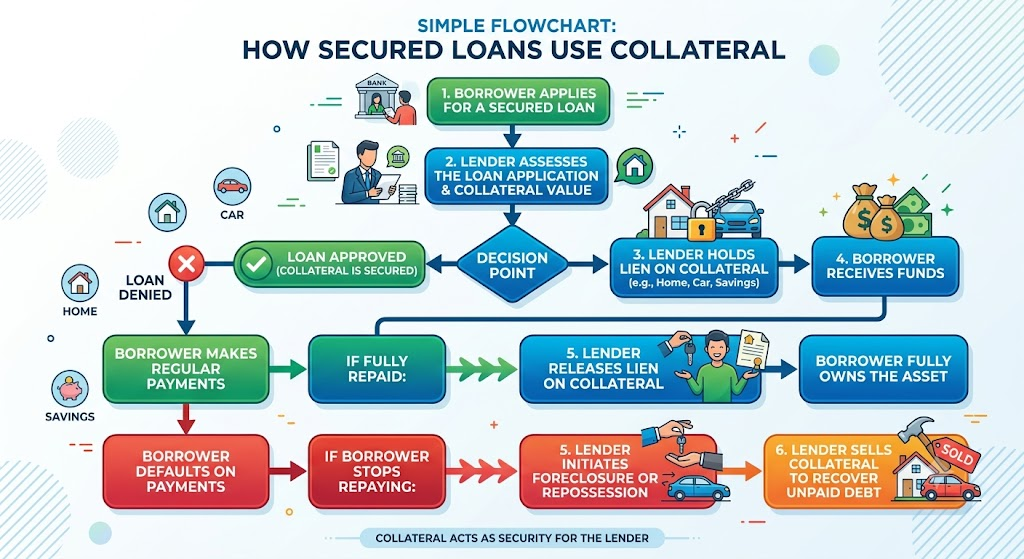

A secured personal loan requires you to provide an asset, also known as collateral, to the lender.

Collateral is something valuable that the lender can claim if you fail to repay the loan according to the agreement.

Common examples of collateral include:

- Savings accounts

- Fixed deposits

- Vehicles

- Property

- Investments

Because the lender has security, secured loans are usually considered less risky for them.

Example

Suppose you need $10,000 and use your car as collateral for a secured personal loan. If you make all payments on time, the loan works normally.

However, if you stop making payments and default on the loan, the lender may have the legal right to take the vehicle to recover the debt.

What Is an Unsecured Personal Loan?

An unsecured personal loan does not require collateral.

Instead, lenders evaluate your:

- Credit score

- Income

- Employment history

- Existing debts

- Overall financial profile

Since there is no collateral involved, lenders take on more risk. As a result, unsecured loans often come with stricter approval requirements and sometimes higher interest rates.

Example

If you apply for a $10,000 unsecured personal loan, the lender reviews your financial information. If approved, you receive the funds without pledging any asset.

Even though no collateral is involved, you are still legally responsible for repaying the loan.

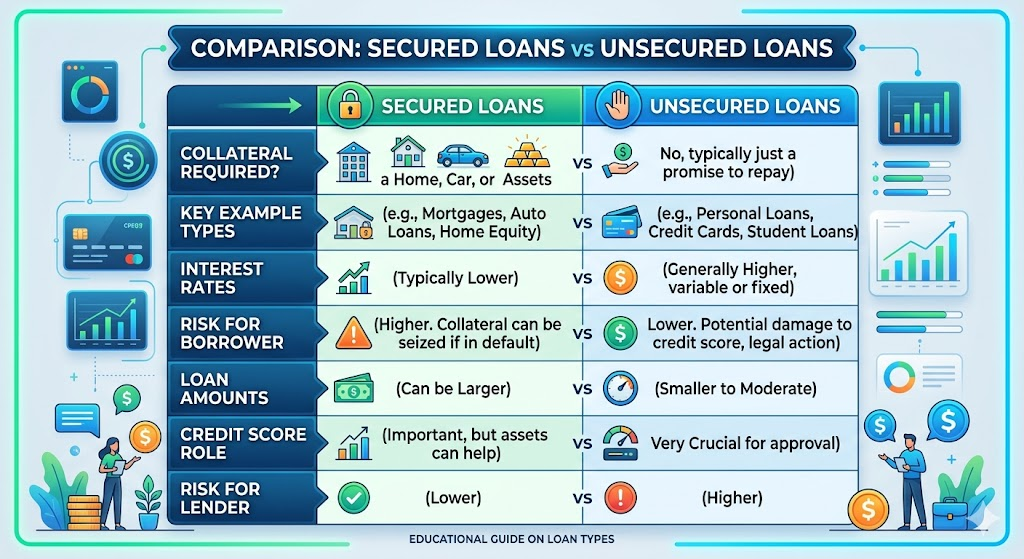

Difference Between Secured and Unsecured Personal Loan

The difference between secured and unsecured personal loan options becomes easier to understand when comparing their key features.

| Feature | Secured Personal Loan | Unsecured Personal Loan |

|---|---|---|

| Collateral Required | Yes | No |

| Approval Requirements | Usually easier | Usually stricter |

| Interest Rates | Often lower | Often higher |

| Loan Amount | May be larger | May be smaller |

| Risk to Borrower | Risk of losing collateral | No asset at risk |

| Credit Score Importance | Moderate | High |

| Processing Time | Sometimes longer | Often faster |

This comparison highlights why borrowers should carefully evaluate both options before applying.

Pros and Cons of Secured Personal Loans

Advantages

Lower Interest Rates

Because lenders have collateral as protection, they may offer lower rates compared to unsecured loans.

Higher Borrowing Limits

Borrowers can often qualify for larger loan amounts.

Easier Approval

People with average or limited credit history may find approval easier if they provide valuable collateral.

Flexible Repayment Options

Some lenders offer longer repayment terms for secured loans.

Disadvantages

Risk of Losing Assets

The biggest disadvantage is that your collateral could be taken if you fail to repay the loan.

Additional Documentation

The lender may require proof of ownership and valuation of the asset.

Longer Approval Process

Verification of collateral can increase processing time.

Pros and Cons of Unsecured Personal Loans

Advantages

No Collateral Needed

You do not need to pledge your home, car, or savings.

Faster Application Process

Many unsecured loans have a simpler approval process.

Lower Personal Risk

Your assets are generally not directly tied to the loan.

Convenient for Emergencies

Borrowers often choose unsecured loans when quick access to funds is important.

Disadvantages

Higher Interest Rates

Lenders usually charge higher rates because they take greater risk.

Stricter Credit Requirements

Applicants with poor credit may find approval more difficult.

Lower Loan Amounts

Some lenders limit borrowing amounts for unsecured loans.

Which Loan Type Is Easier to Get?

In many situations, secured personal loans are easier to obtain because the lender has collateral as protection.

However, approval still depends on factors such as:

- Income stability

- Debt-to-income ratio

- Credit history

- Loan amount requested

Borrowers with strong credit profiles may qualify easily for unsecured loans and enjoy competitive rates.

If you are working on improving your financial profile, consider reading our guide on credit score improvement strategies to understand how lenders evaluate applicants.

Practical Examples

Example 1: Home Renovation

Sarah wants to renovate her home and needs a large loan amount. She uses a fixed deposit as collateral and receives a secured personal loan with a lower interest rate.

Example 2: Emergency Medical Expense

John needs money quickly for an unexpected medical bill. He has a strong credit score and qualifies for an unsecured personal loan without providing collateral.

Example 3: Debt Consolidation

Maria wants to combine multiple debts into one monthly payment. Depending on her credit profile and available assets, either a secured or unsecured loan could be suitable.

Common Mistakes to Avoid

Many borrowers make avoidable mistakes when choosing a loan.

Choosing Based Only on Interest Rate

A lower rate is attractive, but you should also consider the risks involved.

Ignoring Loan Fees

Always review:

- Origination fees

- Late payment fees

- Prepayment penalties

- Administrative charges

Borrowing More Than Necessary

Only borrow what you genuinely need and can comfortably repay.

Not Comparing Multiple Lenders

Different lenders offer different rates, terms, and eligibility requirements.

Forgetting the Risk of Collateral

Before choosing a secured loan, make sure you understand what could happen if repayment becomes difficult.

Helpful Tips Before Applying

Before submitting a loan application, consider these practical tips:

Check Your Credit Report

Review your credit history and correct any errors.

Calculate Your Monthly Budget

Ensure the loan payment fits comfortably within your finances.

Compare Loan Offers

Look beyond interest rates and examine total borrowing costs.

Read the Fine Print

Always understand the loan agreement before signing.

Borrow Responsibly

Only take on debt for legitimate financial needs.

You may also find it useful to explore related topics such as:

- Personal loan eligibility requirements

- Home loan basics for first-time borrowers

- Education loan repayment options

- Banking and finance tips for beginners

These subjects can help you make better long-term financial decisions.

How to Decide Which Loan Is Right for You

A secured personal loan may be suitable if:

- You have collateral available

- You want a lower interest rate

- You need a larger loan amount

- You are comfortable with the collateral risk

An unsecured personal loan may be suitable if:

- You do not want to pledge assets

- You have a strong credit score

- You need funds quickly

- You prefer a simpler application process

The best option depends on your financial goals, repayment ability, and risk tolerance.

Conclusion

Understanding the difference between secured and unsecured personal loan options can help you choose the borrowing solution that fits your needs.

Secured loans generally offer lower rates and higher borrowing limits but require collateral. Unsecured loans do not require assets as security, though they may come with stricter approval requirements and higher interest rates.

Before applying, compare lenders, review the total loan cost, and make sure the monthly payments fit your budget. Taking time to understand your options can help you borrow more confidently and avoid unnecessary financial stress.

Frequently Asked Questions

1. What is the main difference between secured and unsecured personal loans?

A secured loan requires collateral, while an unsecured loan does not.

2. Which type of personal loan usually has lower interest rates?

Secured personal loans often have lower interest rates because the lender has collateral as protection.

3. Can I get an unsecured personal loan with bad credit?

It may be possible, but approval can be more difficult and interest rates may be higher.

4. What happens if I cannot repay a secured loan?

The lender may have the legal right to take the collateral used to secure the loan.

5. Which loan type is better for beginners?

There is no one-size-fits-all answer. The best option depends on your credit profile, available collateral, financial goals, and repayment ability.

Read Also: Common Reasons Why Personal Loan Applications Get Rejected

Leave a Reply