Getting a personal loan is easier when you have a good credit score. In India, most banks and lenders check your CIBIL score before approving a loan application. Many beginners are confused about how much score is needed and whether a low score means automatic rejection.

The good news is that understanding the minimum CIBIL score required for personal loan approval is not very difficult. Once you know how lenders evaluate your credit profile, you can improve your chances of getting approved.

In this guide, we will explain everything in simple language. You will learn what CIBIL score means, the ideal score for personal loans, factors that affect approval, and practical tips to improve your score before applying.

What Is a CIBIL Score?

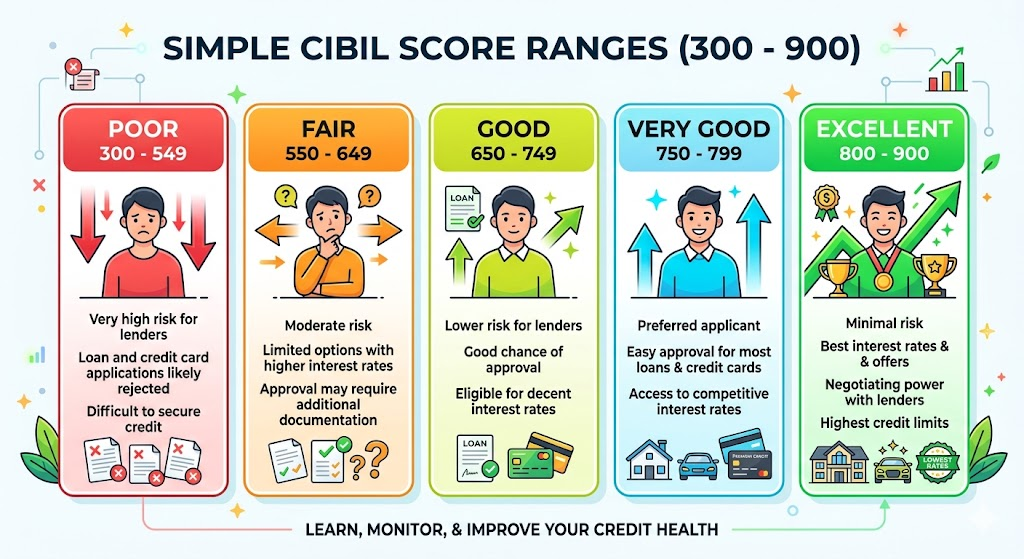

A CIBIL score is a three-digit number that shows your credit history and repayment behavior. The score usually ranges between 300 and 900.

This score is generated by TransUnion CIBIL, one of India’s leading credit bureaus. It helps banks and financial institutions understand whether you are a responsible borrower.

CIBIL Score Range Meaning

| CIBIL Score | Meaning |

|---|---|

| 750 – 900 | Excellent |

| 700 – 749 | Good |

| 650 – 699 | Average |

| 550 – 649 | Low |

| Below 550 | Poor |

A higher score generally increases your chances of getting a personal loan with better interest rates.

Why Is CIBIL Score Important for Personal Loans?

Personal loans are unsecured loans. This means you do not have to provide collateral like property or gold. Because there is no security involved, lenders depend heavily on your credit score.

Your CIBIL score helps lenders understand:

- Your repayment history

- Previous loan behavior

- Credit card payment discipline

- Existing loan burden

- Financial reliability

If your score is good, lenders may see you as a lower-risk borrower.

You can also read related guides on improving your credit profile and understanding how personal loan eligibility works for first-time borrowers.

Minimum CIBIL Score Required for Personal Loan

Most banks and NBFCs in India prefer a CIBIL score of 750 or above for personal loan approval.

However, some lenders may approve loans for applicants with scores between 650 and 749, depending on income, job stability, and existing debts.

Ideal Score for Easy Approval

| Score Range | Loan Approval Chances |

|---|---|

| 750+ | Very High |

| 700 – 749 | Good |

| 650 – 699 | Moderate |

| Below 650 | Difficult |

Although there is no fixed legal minimum score, many lenders become cautious when the score falls below 650.

Why 750 Is Considered Good

A score above 750 usually indicates:

- Timely repayment history

- Good credit management

- Lower risk of default

- Responsible use of credit cards and loans

Because of this, borrowers with higher scores may also get:

- Lower interest rates

- Faster approvals

- Higher loan amounts

- Flexible repayment options

Personal Loan Approval Based on Credit Score

Different lenders may follow different approval policies. Here is a simple idea of what borrowers can expect.

Score Above 750

You are in a strong position. Most banks are likely to consider your application positively.

Score Between 700 and 749

You still have a good chance of approval. However, some lenders may offer slightly higher interest rates.

Score Between 650 and 699

Approval may become difficult with large banks, but some NBFCs may still approve the loan after checking your income and repayment capacity.

Score Below 650

Your options may become limited. Lenders may see you as a higher-risk borrower.

Can You Get a Loan With a Low CIBIL Score?

Yes, getting a loan with a low credit score is possible in some cases, but approval is not guaranteed.

Some lenders may still consider your application if:

- Your monthly income is stable

- You have a secure government or salaried job

- Your debt-to-income ratio is low

- You apply for a smaller loan amount

- You have a co-applicant with a strong credit profile

However, borrowers with low scores often face:

- Higher interest rates

- Lower loan amounts

- Strict eligibility conditions

- Longer approval process

Before applying, it is better to improve your score if possible.

Factors Lenders Check Apart From CIBIL Score

While your credit score is important, lenders also consider other financial details.

Monthly Income

A higher and stable income increases repayment confidence.

Employment Stability

Applicants with long-term jobs or stable businesses may receive better approval chances.

Existing Loans

Too many active loans can reduce your eligibility.

Debt-to-Income Ratio

If a large part of your salary already goes toward EMIs, lenders may hesitate to approve another loan.

Repayment History

Missed EMI or credit card payments negatively affect your profile.

You may also explore guides related to home loan eligibility and education loan repayment planning to better understand how lenders evaluate borrowers.

How to Improve Your CIBIL Score

Improving your score takes time, but small financial habits can make a big difference.

1. Pay EMIs and Credit Card Bills on Time

Late payments can seriously damage your score.

2. Keep Credit Card Usage Low

Experts often recommend using less than 30% of your total credit limit.

3. Avoid Multiple Loan Applications

Too many applications in a short time may reduce your score.

4. Check Your Credit Report Regularly

Errors in your report can affect your score unfairly.

5. Maintain Older Credit Accounts

A longer credit history is usually considered positive.

6. Clear Outstanding Dues

Repaying pending balances can gradually improve your profile.

Common Mistakes to Avoid

Many borrowers unknowingly hurt their credit score through poor financial habits.

Missing Payments

Even a single missed payment can impact your score.

Applying for Too Many Loans

Frequent applications create multiple hard inquiries.

Closing Old Credit Cards Quickly

Older accounts help maintain credit history length.

Ignoring Credit Report Errors

Incorrect information should be corrected immediately.

Using Full Credit Limit

Very high credit utilization may indicate financial stress.

Pros and Cons of High and Low Credit Scores

Benefits of a High CIBIL Score

- Better loan approval chances

- Lower interest rates

- Higher borrowing limits

- Faster processing

- Better credit card offers

Drawbacks of a Low CIBIL Score

- Higher interest costs

- Limited lender options

- Lower approved amount

- Increased verification process

- Possible loan rejection

Tips Before Applying for a Personal Loan

Here are some practical tips beginners should follow.

Compare Multiple Lenders

Interest rates and eligibility rules can vary significantly.

Borrow Only What You Need

Taking unnecessary loans increases repayment burden.

Check Eligibility First

Many lenders provide eligibility calculators online.

Read Loan Terms Carefully

Understand processing fees, EMI amount, penalties, and repayment rules.

Maintain Financial Discipline

Good repayment behavior improves future borrowing opportunities.

If you are new to borrowing, learning the basics of banking and finance can help you make smarter loan decisions.

Conclusion

Understanding the minimum CIBIL score required for personal loan approval can help you prepare better before applying. In most cases, a score of 750 or above is considered ideal because it increases your approval chances and may help you get better interest rates.

However, credit score is not the only factor lenders consider. Your income, repayment history, existing debts, and job stability also play an important role.

If your score is currently low, do not panic. By paying bills on time, reducing debt, and maintaining responsible credit behavior, you can gradually improve your financial profile.

Before applying for any personal loan, always compare lenders carefully and borrow only what you can comfortably repay.

Frequently Asked Questions (FAQs)

1. What is the minimum CIBIL score required for personal loan approval?

Most lenders prefer a score of 750 or above. Some lenders may still consider applicants with scores above 650.

2. Can I get a personal loan with a 600 CIBIL score?

It may be possible with certain NBFCs or private lenders, but approval could come with higher interest rates and stricter conditions.

3. Does checking my CIBIL score reduce it?

Checking your own score does not affect it. However, multiple lender inquiries within a short period may lower your score slightly.

4. How long does it take to improve a CIBIL score?

Improvement usually takes a few months of consistent repayment and responsible credit usage.

5. Is CIBIL score important for all loans?

Yes, most banks check your credit score for personal loans, home loans, education loans, and credit cards.