Getting an education loan can help students pursue higher studies without putting immediate financial pressure on their families. However, many borrowers are confused about one important topic: what happens to the loan interest while they are still studying.

Understanding how interest works during the study period can help you plan your finances better and avoid surprises later. In this guide, we will explain everything in simple language so that even first-time borrowers can understand it easily.

If you are considering a student loan for college, university, or professional courses, this article will help you make informed decisions.

What Is an Education Loan?

An education loan is a type of financial assistance provided by banks and financial institutions to help students pay for higher education expenses.

These expenses may include:

- Tuition fees

- Examination fees

- Hostel charges

- Books and study materials

- Laptop or equipment costs

- Travel expenses for overseas education

The student usually becomes the primary borrower, while a parent or guardian may act as a co-applicant.

What Is the Study Period?

The study period is the time during which a student is actively pursuing the course for which the education loan was taken.

For example:

| Course Duration | Study Period |

|---|---|

| 3-year degree | 3 years |

| 4-year engineering course | 4 years |

| 2-year master’s program | 2 years |

During this period, students are generally focused on their studies and may not have a regular source of income.

Because of this, lenders often provide repayment flexibility.

Education Loan Interest During Study Period Explained

When people hear that education loan repayment starts after studies, they often assume that no interest is charged during that time. This is not correct.

In most cases, interest starts accumulating from the day the loan amount is disbursed.

Even though the borrower may not be required to make full loan repayments immediately, the lender continues to calculate interest on the outstanding amount.

This accumulated interest may either:

- Be paid during the study period, or

- Be added to the loan balance and repaid later

The exact rules depend on the lender’s policies and the type of education loan.

Therefore, it is important to read the loan agreement carefully before signing.

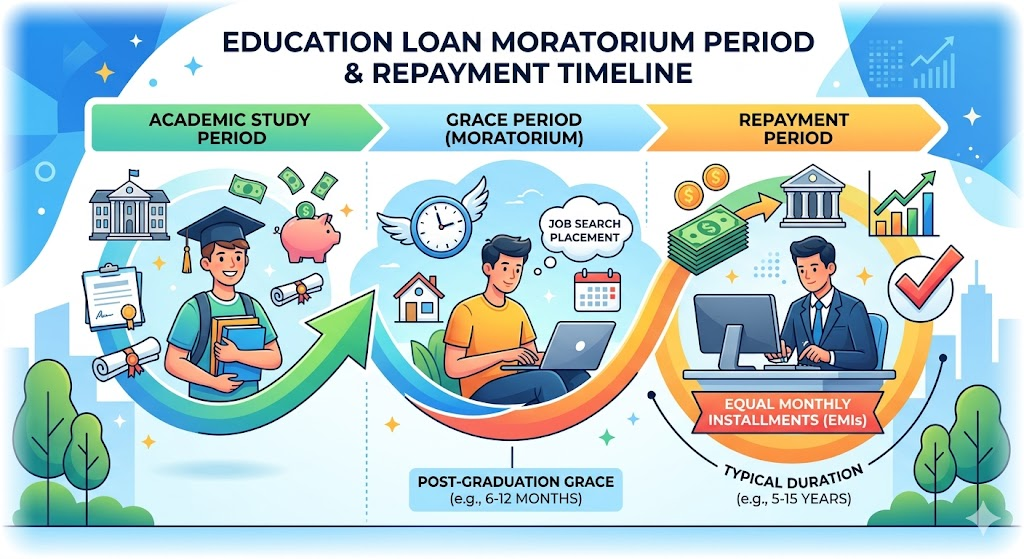

What Is a Moratorium Period?

A moratorium period is a special repayment holiday provided by lenders.

It usually includes:

Course Duration + Additional Grace Period

The grace period is often between 6 and 12 months after course completion, depending on the lender.

The purpose of the moratorium period is to allow students enough time to:

- Complete their education

- Search for a job

- Start earning income

During this period, borrowers may not need to pay full EMIs.

However, interest usually continues to accrue.

How Interest Is Calculated During Studies

Education loan interest is generally calculated on the outstanding loan amount.

Suppose a student receives the loan in installments over several semesters.

Interest is typically charged only on the amount that has already been disbursed.

For example:

- First-year disbursement: ₹2,00,000

- Second-year disbursement: ₹2,00,000

- Third-year disbursement: ₹2,00,000

Interest on the first installment starts earlier because it was released first.

This means that the timing of loan disbursements can affect the total interest payable.

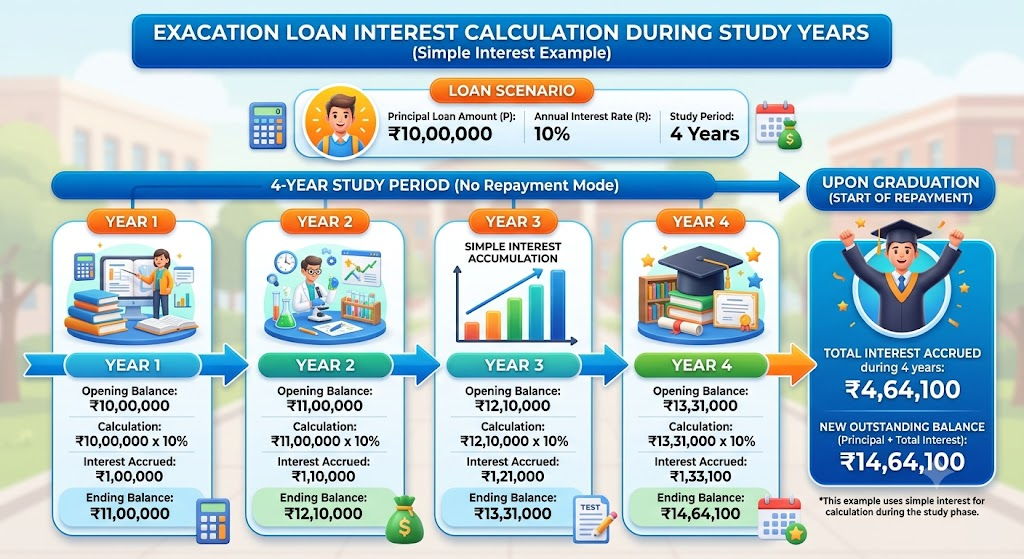

Example of Interest Calculation

Let us understand with a simple example.

| Loan Amount | Interest Rate |

| ₹5,00,000 | 10% per year |

Assume the student does not make any interest payments during a 4-year course.

Interest continues accumulating throughout the study period.

At the end of the course, the borrower may owe:

- Original principal amount

- Accumulated interest

As a result, the total outstanding balance can become significantly higher than the amount originally borrowed.

This is why understanding interest accumulation is so important.

Should You Pay Interest During the Study Period?

Many lenders allow students or their families to voluntarily pay interest while the student is studying.

Although it is not always mandatory, doing so can offer several advantages.

Option 1: Pay Interest During Studies

In this approach:

- Interest is paid regularly

- Principal amount remains unchanged

- Loan balance does not grow significantly

This can reduce the total repayment burden later.

Option 2: Defer Interest Payments

In this approach:

- No interest payments are made during studies

- Interest accumulates over time

- Total loan cost may increase

This option may provide short-term relief but can result in higher repayments later.

The right choice depends on the family’s financial situation.

Benefits of Paying Interest Early

If possible, paying interest during the study period can be a smart financial decision.

Lower Total Interest Cost

Since accumulated interest is reduced, the overall loan becomes cheaper.

Smaller Future EMIs

A lower outstanding balance can lead to more manageable monthly payments after graduation.

Faster Loan Repayment

Borrowers may be able to clear the loan sooner.

Better Financial Discipline

Making small payments early helps students understand loan responsibilities.

Pros and Cons of Deferring Interest Payments

Pros

- No immediate repayment pressure

- More financial flexibility during studies

- Helpful for families with limited income

Cons

- Interest continues accumulating

- Total loan amount may increase

- Future EMIs can become higher

- Loan repayment period may feel longer

Before choosing this option, borrowers should estimate the long-term cost.

Common Mistakes Students Make

Many borrowers make avoidable mistakes because they do not fully understand how education loans work.

Assuming Interest Does Not Apply During Studies

This is one of the most common misconceptions.

Even if repayments are postponed, interest often continues to accumulate.

Ignoring Loan Statements

Students should regularly review loan statements to track outstanding balances.

Not Understanding Moratorium Rules

Every lender may have slightly different policies.

Always confirm:

- When repayment starts

- Whether interest payments are optional or mandatory

- How accumulated interest is treated

Borrowing More Than Necessary

Taking a larger loan than required increases future repayment obligations.

Tips to Reduce Education Loan Costs

Here are some practical ways to manage your education loan effectively:

Borrow Only What You Need

Avoid unnecessary borrowing.

Pay Interest Whenever Possible

Even partial interest payments can make a difference.

Compare Lenders Carefully

Look beyond interest rates and check:

- Processing fees

- Moratorium benefits

- Repayment flexibility

Start Repayment Early

If you secure a part-time job or internship, consider making voluntary payments.

Maintain a Good Credit Profile

A strong credit history can help with future financial products and refinancing opportunities.

Internal Resources You May Find Helpful

To improve your overall financial knowledge, you may also want to explore related topics on LoanApply-For:

- A beginner’s guide to personal loans and how they differ from education loans.

- Understanding credit scores and why they matter for future borrowing.

- Basic banking and finance concepts that every student should know before taking a loan.

You can also compare education loans with other borrowing options such as home loans when planning long-term financial goals.

Conclusion

We hope this guide on education loan interest during study period explained has helped you understand how student loan interest works before repayment officially begins.

The most important thing to remember is that interest generally starts accumulating from the time the loan is disbursed, even if you are still studying. While lenders often provide a moratorium period, this does not always mean that interest stops.

Before taking an education loan, carefully review the terms, understand the repayment structure, and consider paying interest during the study period if your budget allows. Small financial decisions today can make loan repayment much easier after graduation.

Frequently Asked Questions (FAQs)

1. Do education loans charge interest during the study period?

Yes. In most cases, interest starts accruing from the date the loan amount is disbursed, even while the student is studying.

2. What is a moratorium period in an education loan?

A moratorium period is the course duration plus an additional grace period during which full loan repayment is usually postponed.

3. Is it compulsory to pay interest during studies?

Not always. Some lenders allow borrowers to postpone interest payments until after the study period.

4. Does paying interest during the study period help?

Yes. Paying interest early can reduce the overall loan cost and may result in lower future EMIs.

5. What happens if I do not pay interest during my course?

The unpaid interest may accumulate and increase the total amount you must repay after graduation.

Read Also: Best Time to Apply for Education Loan Before Admission

Leave a Reply